Tax Filing Deadlines for Small Businesses in 2025: Navigating the complexities of tax season can be challenging for small business owners. Understanding the specific deadlines for your business structure – sole proprietorship, partnership, LLC, or S corporation – is crucial to avoid penalties. This guide provides a clear overview of these deadlines, the implications of late filing, and helpful strategies for year-round tax planning.

We’ll explore the differences in tax forms, the process of requesting extensions, and common deductions available to help streamline your tax preparation. We’ll also cover valuable resources, including tax software options and government websites, to assist you in this process. By understanding these key aspects, you can approach tax season with confidence and ensure compliance.

Overview of 2025 Tax Filing Deadlines for Small Businesses

Navigating the tax landscape as a small business owner can be complex, especially when it comes to understanding the various filing deadlines. This overview provides a summary of key deadlines for 2025, clarifying the differences between various business structures. Remember that these are general guidelines, and specific circumstances may require consulting with a tax professional.

The Internal Revenue Service (IRS) sets the general tax deadlines, but the specific due date for your business depends on its legal structure (sole proprietorship, partnership, LLC, S corporation) and whether you’re filing estimated taxes or an annual return. Penalties for late filing can be substantial, so accurate and timely filing is crucial.

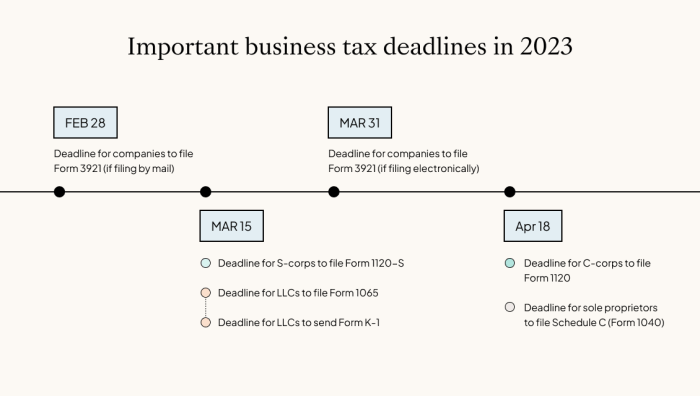

2025 Tax Filing Deadlines for Different Business Structures

The following table summarizes the key tax filing deadlines for different small business structures in 2025. Note that these dates are subject to change, so always verify with the IRS website closer to the filing period.

| Business Structure | Annual Return Due Date | Estimated Tax Quarterly Payments Due | Penalty for Late Filing |

|---|---|---|---|

| Sole Proprietorship (Schedule C) | April 15, 2025 | April 15, June 16, September 15, January 15, 2025 | Interest and penalties on unpaid taxes. |

| Partnership (Form 1065) | March 15, 2025 | Generally not required for partnerships, but partners may need to make estimated tax payments. | Interest and penalties on unpaid taxes. |

| LLC (Depending on Classification) | Varies (April 15th, March 15th, or other dates depending on how the LLC is structured for tax purposes – as a sole proprietorship, partnership, S corp, or disregarded entity) | Varies depending on classification (see above) | Interest and penalties on unpaid taxes. |

| S Corporation (Form 1120-S) | March 15, 2025 | April 15, June 16, September 15, January 15, 2025 (for shareholders) | Interest and penalties on unpaid taxes. |

Comparison of Deadlines: Estimated Taxes vs. Annual Returns

A key distinction lies between estimated taxes and annual tax returns. Estimated taxes are quarterly payments made throughout the year to cover your projected tax liability. Annual returns are filed at the end of the tax year to reconcile your actual income and expenses against your estimated tax payments.

For example, a sole proprietor might estimate their tax liability for the year and make quarterly payments on April 15th, June 16th, September 15th, and January 15th. They would then file their annual return (Schedule C) by April 15th of the following year. Failure to pay estimated taxes on time can result in penalties.

Impact of Business Type on Tax Deadlines

The legal structure of your small business significantly impacts your tax filing deadlines and the complexity of your tax preparation. Choosing the right structure—sole proprietorship, partnership, LLC, or S corporation—has profound implications for how and when you file your taxes. Understanding these differences is crucial for timely and accurate tax compliance.

The primary difference stems from the legal distinction between the business and its owner(s). Sole proprietorships and partnerships blend the business and personal finances, while LLCs and S corporations offer varying degrees of separation. This separation affects both the tax forms used and the overall complexity of tax preparation.

Tax Forms Required for Different Business Structures

The choice of business structure directly determines which tax forms you’ll need to file. Sole proprietors report business income and expenses on Schedule C of Form 1040, their personal income tax return. Partnerships file Form 1065, U.S. Return of Partnership Income, while partners report their share of the partnership’s income on their individual Form 1040. LLCs, depending on how they’re classified by the IRS (as a sole proprietorship, partnership, S corp, or disregarded entity), will utilize different forms. S corporations file Form 1120-S, U.S. Income Tax Return for an S Corporation, distributing profits and losses to shareholders, who then report their share on their individual tax returns.

Complexity of Tax Preparation by Business Type

The complexity of tax preparation varies considerably across different business structures.

- Sole Proprietorship: Generally considered the simplest. Business income and expenses are integrated with personal taxes on Schedule C. This straightforward approach simplifies filing but offers less tax planning flexibility.

- Partnership: More complex than sole proprietorships. The partnership files Form 1065, and each partner reports their share of income and losses on their individual returns. This requires careful tracking of partnership income and distributions.

- LLC: Complexity depends on how the LLC is classified by the IRS. If treated as a disregarded entity or sole proprietorship, it’s relatively simple. If structured as a partnership or S corp, the complexity increases accordingly.

- S Corporation: Generally the most complex. Form 1120-S requires detailed accounting of income, expenses, and distributions to shareholders. This structure allows for potential tax advantages but necessitates more meticulous record-keeping and professional tax assistance.

Extensions and Penalties for Late Filing

Navigating the complexities of small business tax filing can be challenging, and occasionally, unforeseen circumstances may prevent timely submission. Understanding the process for requesting extensions and the potential penalties for late filing is crucial for responsible tax compliance. This section clarifies the procedures and consequences associated with late tax filings for small businesses in 2025.

The process for obtaining an extension to file your small business taxes in 2025 involves filing Form 7004, “Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns.” This form requests an automatic six-month extension, granting you until October 15, 2025, to file your return. It’s important to note that while this extension gives you more time to file, it does *not* extend the deadline for paying your estimated taxes. You are still required to pay any taxes owed by the original April 15, 2025 deadline to avoid accruing penalties and interest. Failure to file the Form 7004 by the original deadline will result in penalties. The IRS provides detailed instructions on their website for completing and submitting this form.

Penalties for Late Filing and Late Payment

Late filing and late payment of taxes result in significant financial penalties. The penalties are calculated based on the amount of unpaid tax and the length of the delay. For late filing, a penalty is generally assessed as a percentage of the unpaid tax. This percentage increases the longer the return is overdue. Additionally, interest accrues on the unpaid tax from the original due date until the tax is fully paid. The interest rate is adjusted periodically by the IRS and is typically higher than standard savings account interest rates. Late payment penalties are also assessed as a percentage of the unpaid tax and increase over time. It is crucial to understand that both penalties are applied separately, meaning you will face both a late filing penalty and a late payment penalty if you fail to file and pay on time.

Examples of Late Filing Penalties

The following table illustrates various scenarios of late filing and their corresponding penalties. These are simplified examples and do not include all possible factors that could affect the actual penalty amounts. Consult a tax professional or the IRS website for the most up-to-date and precise information. Note that these examples assume a hypothetical unpaid tax amount of $10,000. Actual penalties will vary based on the unpaid tax amount and the length of the delay.

| Scenario | Days Late | Late Filing Penalty (Approximate) | Late Payment Penalty (Approximate) |

|---|---|---|---|

| Filed 30 days late, paid on time | 30 | $0 (assuming timely payment) | $0 |

| Filed 60 days late, paid on time | 60 | $500 (5% of $10,000) | $0 |

| Filed 90 days late, paid 30 days late | 90 (Filing) / 30 (Payment) | $750 (7.5% of $10,000) | $250 (2.5% of $10,000) |

| Filed 120 days late, paid 90 days late | 120 (Filing) / 90 (Payment) | $1000 (10% of $10,000) | $750 (7.5% of $10,000) |

Common Tax Deductions for Small Businesses

Understanding available tax deductions is crucial for minimizing your tax liability as a small business owner. Several deductions can significantly reduce your taxable income, making it essential to familiarize yourself with the most common options. Properly claiming these deductions requires careful record-keeping and a thorough understanding of the relevant tax laws.

Home Office Deduction

The home office deduction allows you to deduct expenses related to the portion of your home used exclusively and regularly for business. This includes a portion of mortgage interest, rent, utilities, repairs, and depreciation. To qualify, the home office must be your principal place of business or a place used exclusively and regularly for meeting clients or customers.

For example, if you use 10% of your home for your business and your total home-related expenses are $10,000, you can deduct $1,000 ($10,000 x 10%). It’s important to accurately determine the percentage of your home used for business purposes. The IRS provides detailed guidelines on calculating this percentage. Keep thorough records of all home-related expenses, separating business and personal use.

Qualified Business Income (QBI) Deduction

The QBI deduction allows eligible self-employed individuals, partners, and S corporation shareholders to deduct up to 20% of their qualified business income (QBI). QBI generally includes income, gains, deductions, and losses from a business. However, it excludes certain items like capital gains and losses, and dividends. The deduction is subject to limitations based on taxable income.

Let’s say a sole proprietor has a QBI of $50,000 and a taxable income (before the QBI deduction) of $60,000. In this scenario, they can deduct 20% of their QBI, which is $10,000 ($50,000 x 0.20). This reduces their taxable income to $50,000. However, limitations may apply depending on the taxpayer’s taxable income and business type. Consult the IRS guidelines for detailed calculations and limitations.

Self-Employment Tax Deduction

Self-employed individuals pay self-employment taxes, which cover Social Security and Medicare taxes. These taxes are equivalent to both the employer and employee portions of payroll taxes for employees of larger companies. The self-employed can deduct one-half of their self-employment tax from their gross income.

For instance, if a self-employed individual’s self-employment tax is $10,000, they can deduct $5,000 ($10,000 / 2). This deduction reduces their taxable income, lowering their overall tax liability. It’s crucial to accurately calculate self-employment tax to claim this deduction correctly.

Flowchart for Claiming Deductions

A flowchart illustrating the steps to claim these deductions would visually represent the process. The flowchart would begin with gathering necessary documentation (receipts, invoices, etc.), followed by calculating each deduction (home office, QBI, self-employment tax) according to the relevant rules and limitations. The next step would involve preparing the tax return, inputting the calculated deductions into the appropriate sections, and finally, filing the tax return with all supporting documentation. Each step would be represented by a box in the flowchart with arrows indicating the sequence of actions.

Tax Software and Resources for Small Businesses: Tax Filing Deadlines For Small Businesses In 2025

Navigating the complexities of small business taxes can be daunting, but thankfully, numerous resources and tools are available to simplify the process. Choosing the right approach, whether using tax software or engaging a professional, significantly impacts accuracy and efficiency. This section explores various options and resources to assist small business owners in meeting their tax obligations.

Choosing the right tax preparation method depends heavily on your comfort level with accounting, the complexity of your business finances, and your available budget. Careful consideration of these factors will help you make an informed decision.

Reputable Tax Software Options for Small Businesses

Several reputable software options cater specifically to the needs of small businesses, offering varying levels of features and pricing. These programs often automate calculations, provide guidance, and help generate the necessary tax forms.

- TurboTax Self-Employed: This popular option offers comprehensive features for independent contractors and small business owners, including scheduling C, 1099 reporting, and expense tracking. Pricing varies depending on the chosen plan, generally ranging from $100 to $200. It offers excellent user support and a relatively intuitive interface.

- H&R Block Premium & Business: Similar to TurboTax, H&R Block provides a robust platform for small business tax preparation. It also includes features for self-employment taxes, expense tracking, and various business-specific forms. Pricing is comparable to TurboTax, usually falling within the same price range.

- QuickBooks Self-Employed: Primarily known for its accounting software, QuickBooks also offers a tax solution integrated with its accounting features. This seamless integration makes it particularly appealing to users already utilizing QuickBooks for their bookkeeping. Pricing typically falls in line with other major tax software providers.

- TaxAct Self-Employed: TaxAct offers a more budget-friendly alternative, providing many of the essential features found in more expensive options. While features may be slightly less extensive, it’s a viable choice for those seeking a cost-effective solution. Pricing is generally lower than TurboTax or H&R Block.

Professional Tax Preparers vs. Self-Preparation

The decision of whether to hire a professional tax preparer or prepare your taxes yourself involves weighing several factors.

- Professional Tax Preparers: Advantages include expertise in tax law, reduced risk of errors, and time savings. Disadvantages are the higher cost and relinquishing some control over the process. A qualified professional can navigate complex tax situations and potentially identify deductions you might miss.

- Self-Preparation: Advantages include cost savings and greater control over the process. Disadvantages include the risk of errors, the need for tax knowledge, and the time investment required. Using tax software can mitigate some of these disadvantages, but it still requires understanding tax laws and regulations.

Free Online Resources and Government Websites

The IRS and other government agencies offer valuable free resources to assist small business owners with their tax obligations. Utilizing these resources can provide significant support and guidance.

- IRS Website (irs.gov): The official IRS website is an invaluable resource, providing access to publications, forms, instructions, and frequently asked questions. It’s a primary source for accurate and up-to-date tax information.

- Small Business Administration (SBA) Website (sba.gov): The SBA offers resources and guidance on various aspects of running a small business, including financial management and tax planning. Their website provides links to relevant IRS information and other helpful resources.

- Tax Counseling for the Elderly (TCE): TCE offers free tax help to seniors and others, particularly those with low to moderate incomes. They provide assistance with tax preparation and related questions.

- AARP Foundation Tax-Aide: Similar to TCE, Tax-Aide provides free tax assistance to taxpayers of all ages, with a focus on those with low and moderate incomes. They offer in-person and virtual assistance.

Preparing for Tax Season

Effective year-round tax planning is crucial for small businesses, minimizing stress during tax season and potentially maximizing tax benefits. Proactive strategies throughout the year can significantly simplify the process and ensure compliance. This involves diligent record-keeping, strategic financial management, and utilizing available resources.

Strategic tax planning isn’t just about filing taxes efficiently; it’s about proactively managing your business finances to minimize your tax liability throughout the year. This involves understanding your business structure, allowable deductions, and making informed financial decisions that align with your tax obligations.

Maintaining Accurate Records and Utilizing Accounting Software

Maintaining detailed and organized financial records is paramount for accurate tax preparation. This includes meticulous tracking of income and expenses, invoices, receipts, bank statements, and all other relevant financial documents. Utilizing accounting software can automate many of these tasks, providing real-time insights into your financial performance and simplifying the process of generating financial reports needed for tax filing. Software options range from simple spreadsheet programs to sophisticated cloud-based accounting systems, offering features like automated expense tracking, invoice generation, and financial reporting. Choosing the right software depends on the size and complexity of your business. For example, a sole proprietor might find a simple spreadsheet sufficient, while a larger business might require a more comprehensive system with inventory management capabilities.

Separating Business and Personal Finances

Keeping business and personal finances completely separate is essential for accurate tax reporting and simplifies the auditing process. Mixing funds can lead to confusion, inaccuracies, and potential penalties. This separation should extend to bank accounts, credit cards, and all financial transactions. Using dedicated business bank accounts and credit cards simplifies the tracking of business expenses and income, providing a clear audit trail for tax purposes. This separation also helps to protect personal assets in the event of business-related liabilities. Failing to maintain this separation can make it difficult to accurately determine your business’s profits and losses, resulting in inaccurate tax filings.

Year-Round Tax Preparation Checklist, Tax Filing Deadlines for Small Businesses in 2025

Regularly performing these tasks throughout the year will significantly ease the tax preparation burden.

A well-structured checklist helps streamline the process. Consider these key tasks:

- Monthly: Reconcile bank statements, categorize expenses, pay estimated taxes.

- Quarterly: File estimated tax payments (if applicable), review financial statements for accuracy.

- Annually: Conduct a year-end review of financial records, gather all necessary tax documents, and consult with a tax professional.

Illustrative Example: Sarah’s Small Business Tax Scenario

This example follows Sarah, a freelance graphic designer, through the process of filing her 2024 taxes. We’ll examine her income, deductions, and the calculation of her tax liability, illustrating a common scenario for small business owners. This will provide a practical understanding of the tax filing process.

Sarah, operating as a sole proprietor, earned $60,000 in 2024 from her graphic design services. She also had $5,000 in business expenses, including software subscriptions, marketing costs, and office supplies. Additionally, she contributed $6,000 to a self-employed retirement plan (SEP IRA).

Income Calculation

Sarah’s total income for the year is $60,000. This figure represents the gross revenue from her graphic design work. No other income sources are considered in this example.

Deduction Calculation

Sarah can deduct several business expenses. Her total business expenses are $5,000. Furthermore, she can deduct the $6,000 contribution to her SEP IRA, as this is a legitimate deduction for self-employed individuals. Therefore, her total deductions amount to $11,000 ($5,000 + $6,000).

Tax Liability Calculation

To determine Sarah’s tax liability, we first calculate her net income. This is done by subtracting her total deductions from her gross income: $60,000 (Gross Income) – $11,000 (Total Deductions) = $49,000 (Net Income). Using the appropriate tax brackets for 2024 (hypothetical example for illustration purposes, consult official IRS tax brackets for the accurate rates), let’s assume a simplified tax rate of 20% on this net income. Therefore, her estimated tax liability would be $9,800 ($49,000 x 0.20). This is a simplified calculation and does not include potential adjustments or credits that might reduce her overall tax liability.

Completing Relevant Tax Forms

Sarah will primarily use Schedule C (Profit or Loss from Business) to report her business income and expenses. She will also use Form 1040, U.S. Individual Income Tax Return, to report her total income and calculate her tax liability. Form 5329, Additional Taxes on Qualified Retirement Plans, etc., will be used to report her SEP IRA contributions.

Step-by-Step Filing Process

- Gather all necessary documents: This includes income statements, expense receipts, and bank statements related to her business.

- Complete Schedule C: Sarah will meticulously record her business income and expenses on Schedule C, ensuring accuracy and proper categorization.

- Complete Form 1040: She will transfer the net profit or loss from Schedule C to Form 1040.

- Complete Form 5329 (if applicable): Sarah will report her SEP IRA contributions on this form.

- Review and double-check: Before filing, Sarah should thoroughly review all completed forms for accuracy and completeness.

- File electronically or by mail: Sarah can file her taxes electronically using tax software or mail her completed forms to the IRS.

Epilogue

Successfully navigating tax season requires proactive planning and a thorough understanding of relevant deadlines and regulations. By utilizing the resources and strategies Artikeld in this guide, small business owners can streamline their tax preparation process, minimize potential penalties, and focus on the continued growth and success of their ventures. Remember, proactive year-round tax planning is key to a smoother tax season.

Question & Answer Hub

What happens if I file my taxes late?

Late filing results in penalties and interest charges on any unpaid taxes. The penalties increase depending on how late the filing is.

Can I deduct my home office expenses?

Yes, if you use a portion of your home exclusively and regularly for business, you can deduct a portion of expenses like mortgage interest, utilities, and rent.

What is the Qualified Business Income (QBI) deduction?

The QBI deduction allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

Where can I find reliable tax software?

Several reputable tax software options cater to small businesses, offering varying features and pricing. Research options like TurboTax Self-Employed, H&R Block Premium & Business, or TaxAct Self-Employed.