Personal Budgeting vs Business Budgeting: While both involve managing finances, the approaches, goals, and complexities differ significantly. Personal budgeting focuses on individual financial well-being, managing income and expenses to achieve personal goals like saving for a house or retirement. Business budgeting, conversely, is a crucial strategic tool for companies, guiding resource allocation, forecasting profitability, and ensuring long-term viability. This exploration delves into the core distinctions, highlighting the unique challenges and rewards of each.

Understanding these differences is critical for both individuals and entrepreneurs. Effective personal budgeting leads to financial stability and freedom, while successful business budgeting drives growth and sustainable profitability. This comparison will illuminate the key aspects of each, providing a framework for effective financial management in both personal and professional life.

Defining Personal vs. Business Budgeting

Personal and business budgeting, while both involving the careful management of financial resources, differ significantly in their goals, methods, and key performance indicators. Personal budgeting focuses on managing individual or household income and expenses to achieve financial stability and meet personal goals, while business budgeting aims to optimize resource allocation, track performance, and ensure profitability for an organization. The fundamental differences stem from the distinct objectives and the nature of the financial flows involved.

Personal budgeting and business budgeting employ different approaches to financial planning and control. The primary distinctions lie in the scale of operations, the complexity of financial transactions, and the ultimate objectives being pursued. Personal budgets are generally simpler, reflecting individual needs and aspirations, while business budgets are more intricate, incorporating projections for revenue, expenses, and investments, all contributing to the overarching goal of maximizing shareholder value.

Personal Budgeting Methods

Several common methods help individuals manage their finances effectively. These methods provide a framework for tracking income and expenses, allowing individuals to identify areas for potential savings and make informed financial decisions. The choice of method often depends on individual preferences and financial complexity.

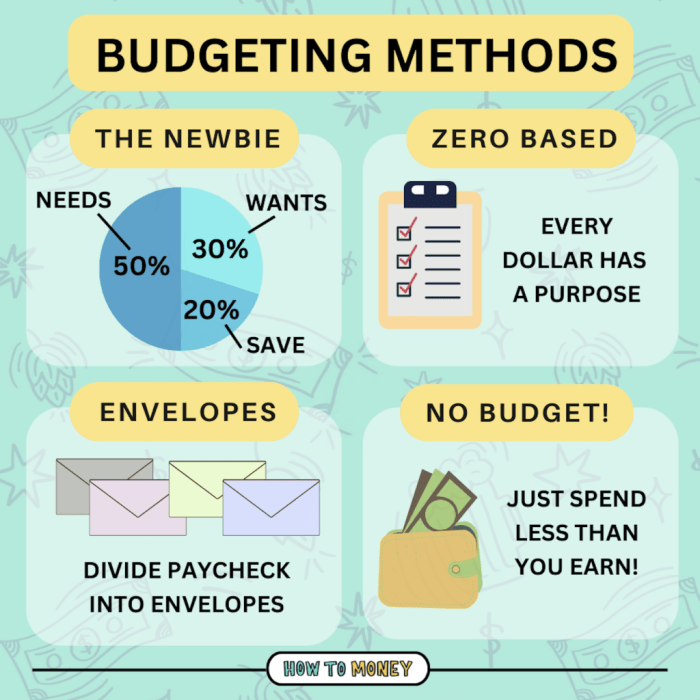

- Zero-Based Budgeting: This method allocates every dollar of income to a specific expense category, ensuring that all income is accounted for and that spending doesn’t exceed earnings. For example, an individual might allocate portions of their income to housing, transportation, food, savings, and entertainment, leaving a zero balance at the end of the budgeting period.

- 50/30/20 Budget: This popular method divides after-tax income into three categories: 50% for needs (housing, utilities, groceries), 30% for wants (entertainment, dining out), and 20% for savings and debt repayment. A person earning $5,000 after tax would allocate $2,500 to needs, $1,500 to wants, and $1,000 to savings and debt repayment.

- Envelope System: This cash-based method involves assigning physical envelopes to different expense categories and allocating a set amount of cash to each. Once the cash in an envelope is spent, that category’s spending is complete for the period. This method can be particularly effective for visual learners and those who want to avoid overspending.

Business Budgeting Methods

Businesses utilize various budgeting methods to forecast financial performance and manage resources effectively. The choice of method depends on factors like the business’s size, industry, and stage of development. These methods provide a roadmap for financial planning and control, enabling businesses to make data-driven decisions.

- Incremental Budgeting: This method starts with the previous year’s budget and adjusts it based on anticipated changes in revenue, expenses, or other factors. For example, a company might increase its marketing budget by 10% based on projected sales growth.

- Zero-Based Budgeting: Similar to its personal finance counterpart, this approach requires justifying every expense from scratch each budgeting period. Every line item must be evaluated and approved, regardless of past spending patterns. This can be particularly useful for identifying and eliminating unnecessary expenses.

- Activity-Based Budgeting: This method links expenses directly to specific activities or projects. This allows for more accurate cost allocation and performance tracking. For instance, a manufacturing company might track the cost of materials, labor, and overhead associated with each product line.

Key Performance Indicators (KPIs) in Personal Budgeting

Personal budgeting KPIs focus on achieving financial goals and maintaining financial health. Regular monitoring of these indicators provides valuable insights into financial progress and helps identify areas needing improvement.

- Net Worth: The difference between assets (what you own) and liabilities (what you owe).

- Savings Rate: The percentage of income saved each month or year.

- Debt-to-Income Ratio: The ratio of total debt payments to gross income.

- Emergency Fund Progress: The amount saved towards an emergency fund, typically 3-6 months of living expenses.

Key Performance Indicators (KPIs) in Business Budgeting

Business budgeting KPIs provide a measure of the organization’s financial health and performance against its goals. These indicators help businesses make informed decisions and track progress toward strategic objectives.

- Revenue Growth: The percentage increase or decrease in revenue over a specific period.

- Profit Margin: The percentage of revenue remaining after deducting all expenses.

- Return on Investment (ROI): A measure of the profitability of an investment.

- Cash Flow: The movement of cash into and out of the business.

Income and Expense Tracking

Effective income and expense tracking is crucial for both personal and business financial health. While the fundamental principle remains the same – monitoring money coming in and going out – the methods, complexity, and required detail differ significantly between personal and business budgeting. This section will explore these differences.

Personal and business budgeting both necessitate meticulous record-keeping of income and expenses. However, the level of detail and formality varies considerably. Personal budgeting often relies on simpler methods, while business budgeting requires a more robust and formal approach due to legal and tax implications.

Typical Income Sources

The sources of income for personal and business budgets differ substantially. Personal income typically stems from employment, investments, and other sources, while business income is derived from sales, services, and investments related to the business. The following tables illustrate typical examples.

Discover more by delving into Common Financial Statement Errors and Fixes further.

| Personal Income Sources | Business Income Sources |

|---|---|

| Salary/Wages | Sales Revenue |

| Investment Income (Dividends, Interest) | Service Revenue |

| Rental Income | Investment Income |

| Freelance/Gig Work | Other Income (e.g., grants, royalties) |

Typical Expense Categories

Similarly, the categories of expenses differ between personal and business budgets. Personal expenses focus on daily living costs, while business expenses encompass operational costs, marketing, and other business-related expenditures. The following table provides a comparison.

| Personal Expense Categories | Business Expense Categories |

|---|---|

| Housing (Rent/Mortgage) | Cost of Goods Sold (COGS) |

| Food | Salaries & Wages |

| Transportation | Rent/Mortgage (Business Premises) |

| Utilities | Marketing & Advertising |

| Healthcare | Office Supplies |

| Entertainment | Professional Services |

| Debt Repayment | Insurance |

Software and Tools for Income and Expense Tracking

A variety of software and tools are available to assist with income and expense tracking, catering to both personal and business needs. The choice often depends on the complexity of the budget, the level of detail required, and the user’s technical proficiency.

For personal budgeting, simple spreadsheet software like Microsoft Excel or Google Sheets can be effective. Many free mobile apps also offer budgeting features, often incorporating expense tracking through automated bank account linking. These apps often provide visual representations of spending patterns, making it easier to identify areas for improvement.

Business budgeting often requires more sophisticated software, such as accounting software packages like QuickBooks, Xero, or FreshBooks. These programs offer features like invoice generation, expense categorization, and financial reporting, which are essential for managing a business’s finances effectively and complying with tax regulations. They frequently integrate with bank accounts and credit card statements for automated data entry, streamlining the tracking process.

Budgeting Goals and Objectives

Effective budgeting, whether personal or business-oriented, hinges on clearly defined goals and objectives. These goals provide a roadmap for financial decisions, ensuring resources are allocated strategically to achieve desired outcomes. Understanding the distinctions in goals between personal and business budgeting is crucial for successful financial management.

Personal Budgeting Goals and Objectives

Personal budgeting primarily focuses on achieving financial security and well-being. This involves managing current expenses while planning for future needs and aspirations. Goals are often shorter-term, addressing immediate needs and medium-term objectives, such as debt reduction or saving for a down payment. Long-term goals might include retirement planning or funding a child’s education.

Business Budgeting Goals and Objectives

Business budgeting, conversely, aims to maximize profitability and ensure the long-term sustainability of the enterprise. Objectives are multifaceted, encompassing revenue generation, cost control, and efficient resource allocation. Time horizons are typically longer, with budgets often extending over several years, encompassing short-term operational needs alongside long-term strategic investments and growth initiatives. Forecasting future revenue streams and managing potential risks are central to business budgeting.

Time Horizons in Personal vs. Business Budgets, Personal Budgeting vs Business Budgeting

Personal budgets often operate on shorter timeframes, with monthly or yearly cycles being common. Individuals might create a monthly budget to track expenses and ensure sufficient funds for necessities. Longer-term personal financial plans, like retirement savings, are typically reviewed annually or less frequently. Business budgets, however, often span several years, incorporating both short-term operational plans and long-term strategic goals. A company might have a yearly operating budget, a three-year strategic plan, and a five-year capital expenditure budget. This allows for flexibility in adapting to changing market conditions while maintaining a clear path towards long-term objectives.

Common Financial Goals for Individuals and Businesses

The following table illustrates common financial goals for individuals and businesses, highlighting the differences in their focus and approach.

| Goal | Individual | Business |

|---|---|---|

| Emergency Fund | Building a savings account to cover unexpected expenses (e.g., medical bills, job loss). A common target is 3-6 months of living expenses. | Maintaining sufficient cash reserves to handle unexpected downturns or market fluctuations. |

| Debt Reduction | Paying off high-interest debt, such as credit card balances, to reduce financial burden and improve credit score. | Managing debt levels, optimizing financing strategies, and maintaining a healthy debt-to-equity ratio. |

| Savings & Investments | Saving for large purchases (e.g., house, car) and investing for retirement or long-term goals. | Investing in research and development, expanding operations, and acquiring new assets to fuel growth and increase profitability. |

| Homeownership | Saving for a down payment and securing a mortgage to purchase a home. | Acquiring and maintaining property necessary for business operations. |

| Retirement Planning | Contributing to retirement accounts (e.g., 401(k), IRA) to secure financial stability during retirement. | Implementing strategies for long-term sustainability, succession planning, and ensuring the continued profitability of the business beyond the current leadership. |

Budgeting Techniques and Strategies

Effective budgeting relies on employing suitable techniques and strategies tailored to the specific context – personal or business. While the fundamental principles remain consistent, the scale, complexity, and objectives differ significantly, leading to variations in approach. This section will explore several key techniques and their application in both personal and business settings.

Zero-Based Budgeting

Zero-based budgeting (ZBB) starts from a baseline of zero for every budget period. Each expense must be justified and approved anew, regardless of its presence in previous budgets. In personal finance, ZBB involves meticulously allocating every dollar of anticipated income to specific categories, ensuring no funds remain unallocated. This promotes mindful spending and prevents overspending. For businesses, ZBB offers a rigorous approach to resource allocation, forcing departments to justify their expenditure needs and potentially uncovering inefficiencies. A small business might use ZBB to allocate funds to marketing, research and development, and operations, justifying each expense based on its projected return on investment. A large corporation might use it to evaluate the performance of different business units and prioritize funding accordingly. The difference lies in the scale and complexity of the process, with personal ZBB often being simpler and less formal than its business counterpart.

Envelope Budgeting and Business Equivalents

Envelope budgeting is a popular personal finance technique involving allocating cash to specific spending categories (e.g., groceries, entertainment) and placing the designated amount in separate envelopes. Once the cash in an envelope is depleted, spending in that category ceases until the next budgeting period. Business equivalents might include the use of dedicated accounts or prepaid cards for specific departmental expenses, preventing overspending and enhancing financial control. For example, a marketing department might receive a pre-set amount each month on a dedicated card, forcing them to manage their budget within those constraints. This is similar in principle to envelope budgeting, but on a larger scale and with more sophisticated tracking mechanisms.

Forecasting Techniques

Forecasting plays a crucial role in both personal and business budgeting. In personal finance, simple forecasting might involve projecting income based on past earnings and anticipated bonuses, while expense projections are based on historical spending patterns. For businesses, more sophisticated techniques are often employed, such as regression analysis to predict sales based on market trends, or time series analysis to identify seasonal patterns in demand. For instance, a restaurant might use historical sales data to forecast demand during peak seasons and adjust staffing levels accordingly. A personal finance example would be projecting holiday spending based on past years’ expenses, allowing for proactive saving. The key difference lies in the sophistication and data analysis used. Businesses typically leverage advanced statistical tools and software, whereas personal finance forecasting is often more intuitive and based on simpler calculations.

Fund Allocation Methods

Fund allocation methods vary significantly between personal and business budgets. Personal budgets often utilize a 50/30/20 rule (50% needs, 30% wants, 20% savings/debt repayment), while others might prioritize specific financial goals (e.g., down payment on a house). Businesses often use more complex allocation methods, such as activity-based costing, which assigns costs to specific business activities to evaluate profitability and efficiency. Capital budgeting techniques, such as net present value (NPV) and internal rate of return (IRR) calculations, are frequently used to evaluate investment opportunities. For example, a business might use NPV to determine whether investing in new equipment is financially viable. A personal finance equivalent might be evaluating the financial viability of purchasing a new car versus investing that money. The difference is in the sophistication of the tools and the complexity of the calculations involved. Businesses need more rigorous methods due to the higher financial stakes.

Financial Forecasting and Projections

Financial forecasting is the process of estimating future financial performance. It’s a crucial element in both personal and business budgeting, allowing for proactive planning and informed decision-making. Accurate forecasting helps individuals and businesses anticipate potential financial challenges and capitalize on opportunities. While the scale and complexity differ, the underlying principles remain consistent.

The Importance of Financial Forecasting in Business Budgeting

Financial forecasting is vital for business success. It provides a roadmap for the future, enabling businesses to secure necessary funding, manage resources effectively, and make strategic decisions based on projected outcomes. Forecasting helps businesses identify potential risks, such as cash flow shortages or declining sales, allowing them to implement mitigating strategies. Furthermore, accurate projections are essential for attracting investors and securing loans, as they demonstrate a clear understanding of the business’s financial trajectory. A well-defined forecast forms the basis for effective business planning and contributes significantly to long-term sustainability.

Personal Budgeting and Short-Term/Long-Term Financial Projections

Incorporating short-term and long-term financial projections into personal budgeting allows for a comprehensive view of financial health. Short-term projections, typically covering a period of one to three months, focus on immediate financial needs and goals, such as paying bills and managing monthly expenses. Long-term projections, spanning several years, help individuals plan for significant life events like purchasing a home, funding education, or retirement. These projections consider factors such as income growth, inflation, and potential investment returns. By combining both short-term and long-term perspectives, individuals can create a realistic and achievable financial plan.

Creating a Simple Personal Budget Projection for the Next Year

To create a simple personal budget projection for the next year, begin by estimating your income for each month. This may involve considering potential salary increases, bonuses, or part-time income. Next, estimate your monthly expenses, categorizing them into essential (housing, food, transportation) and non-essential (entertainment, dining out) spending. Consider potential changes in expenses, such as increased utility costs or planned purchases. Finally, subtract your total estimated expenses from your total estimated income for each month to determine your projected monthly savings or deficit. This process can be easily done using a spreadsheet or budgeting app. For example, if your estimated monthly income is $3,000 and your estimated expenses are $2,500, your projected monthly savings would be $500, resulting in an annual savings of $6,000.

A Hypothetical Business Budget Projection

The following table illustrates a hypothetical one-year business budget projection for a small bakery. This projection considers revenue, various expenses, and profit margins on a quarterly basis. Note that these figures are for illustrative purposes only and do not represent actual business performance.

| Quarter | Revenue | Expenses | Profit Margin |

|---|---|---|---|

| Q1 | $25,000 | $15,000 | 40% |

| Q2 | $30,000 | $18,000 | 40% |

| Q3 | $35,000 | $21,000 | 40% |

| Q4 | $40,000 | $24,000 | 40% |

Risk Management and Contingency Planning

Effective risk management and contingency planning are crucial for both personal and business budgeting, ensuring financial stability and resilience in the face of unexpected events. While the scale and complexity differ, the underlying principles remain remarkably similar. Both require identifying potential threats, assessing their likelihood and impact, and developing strategies to mitigate or avoid them.

Comparing Personal and Business Risk Assessment and Management

Personal risk assessment focuses on individual vulnerabilities, such as job loss, medical emergencies, or unexpected home repairs. Businesses, on the other hand, consider broader risks impacting profitability and sustainability, including market fluctuations, supply chain disruptions, and regulatory changes. Personal risk mitigation often involves building an emergency fund and securing insurance coverage. Business risk management utilizes more sophisticated tools like financial modeling and risk analysis software to identify and assess potential threats, developing strategies such as diversification, hedging, and insurance policies tailored to the specific business needs. Both individuals and businesses benefit from regular reviews and updates to their risk assessments to account for changing circumstances.

Contingency Planning for Unexpected Expenses

Creating a contingency plan involves proactively identifying potential unexpected expenses and establishing a strategy to address them. For individuals, this might involve setting aside a portion of their income in a savings account specifically designated for emergencies. A detailed plan could include specific thresholds for triggering the use of these funds (e.g., job loss, major car repair). Businesses approach this more formally, often incorporating contingency plans into their overall business strategy. This could include setting aside a reserve fund, negotiating flexible credit lines, or having insurance policies that cover various scenarios, such as property damage or business interruption. Regular review and adjustment of these plans are essential to ensure they remain relevant and effective.

Common Financial Risks

Individuals commonly face risks such as unemployment, medical expenses, and unexpected home repairs. Businesses face risks including decreased sales, increased operating costs, and legal liabilities. Both individuals and businesses are vulnerable to inflation and economic downturns, impacting purchasing power and profitability. Cybersecurity threats also pose significant risks to both, potentially leading to financial losses and reputational damage.

Building Financial Resilience

Building financial resilience involves establishing a strong foundation to withstand unexpected financial shocks. For individuals, this includes diversifying income streams, maintaining an emergency fund (ideally 3-6 months of living expenses), and securing adequate insurance coverage. Businesses can enhance resilience by diversifying their customer base, optimizing their supply chain, and investing in robust cybersecurity measures. Regular financial planning and monitoring, coupled with proactive risk management, are essential for both individuals and businesses to build and maintain financial resilience. For example, a business might diversify its product offerings to reduce reliance on a single product line, while an individual might build skills that make them more marketable in the job market.

Analysis and Adjustments

Budgeting isn’t a set-it-and-forget-it process; regular review and adjustment are crucial for both personal and business financial health. Consistent monitoring allows for proactive identification of discrepancies and opportunities for improvement, ultimately leading to better financial outcomes. This section will explore the processes of reviewing and adjusting budgets for both personal and business contexts, emphasizing the importance of regular monitoring and highlighting methods for identifying areas needing improvement.

Regular budget monitoring and analysis is essential for ensuring financial stability and achieving financial goals. Without consistent review, budgets become outdated and ineffective, potentially leading to overspending and unmet objectives. The frequency of review depends on the complexity of the budget and the specific needs of the individual or business. For personal budgets, a monthly review is often sufficient, while businesses may require weekly or even daily monitoring, depending on their size and industry.

Personal Budget Review and Adjustment

The process of reviewing a personal budget typically involves comparing actual spending against the budgeted amounts for each category. This comparison highlights areas of overspending or underspending. For instance, if the budgeted amount for groceries was $500, but actual spending was $600, this indicates a need for adjustment. Possible adjustments include reducing spending in other categories or finding ways to reduce grocery expenses, such as meal planning or utilizing coupons. Significant variances require investigation to identify the root cause and implement corrective actions. This may involve adjusting spending habits, exploring alternative options, or re-evaluating financial goals.

Business Budget Review and Adjustment

Reviewing a business budget is more complex than a personal budget due to the involvement of multiple departments, revenue streams, and expenses. Businesses often utilize sophisticated accounting software to track income and expenses automatically. The process typically involves comparing actual revenues and expenses to the budgeted amounts, analyzing variances, and identifying trends. For example, if marketing expenses are significantly higher than budgeted, the business might investigate the effectiveness of the marketing campaigns and adjust future spending accordingly. Similarly, if sales are lower than projected, the business may need to revise its sales strategies or pricing models. Regular variance analysis allows for timely adjustments and prevents minor issues from escalating into major financial problems.

Methods for Identifying Areas for Improvement

Several methods can be used to pinpoint areas needing improvement in both personal and business budgets. These include analyzing spending patterns, identifying recurring expenses, and comparing performance against industry benchmarks (for businesses). For personal budgets, tracking spending using budgeting apps or spreadsheets can reveal spending habits. For businesses, detailed financial reports, performance dashboards, and key performance indicators (KPIs) provide valuable insights. Identifying areas of inefficiency, waste, or underperformance allows for targeted adjustments and improved resource allocation. For instance, a business might discover that a specific product line is consistently underperforming, prompting a decision to discontinue the product or adjust its pricing and marketing strategies.

Last Recap: Personal Budgeting Vs Business Budgeting

In conclusion, the core difference between personal and business budgeting lies in their ultimate objectives and the scale of operations. Personal budgeting prioritizes individual financial health and long-term security, while business budgeting is a strategic instrument for growth, profitability, and risk mitigation. Mastering both requires discipline, planning, and a clear understanding of financial goals. By employing appropriate techniques and regularly monitoring progress, individuals and businesses alike can achieve their financial aspirations.

Helpful Answers

What is the biggest difference between personal and business budgeting software?

Business budgeting software typically offers more advanced features like forecasting, reporting, and collaboration tools tailored to multiple users and complex financial structures, whereas personal budgeting software prioritizes simplicity and ease of use for individual financial tracking.

Can I use personal budgeting methods for a small business?

For very small businesses, some personal budgeting methods might suffice initially. However, as the business grows, more sophisticated business budgeting techniques and software will likely be necessary to manage increasing complexity and scale.

How often should I review and adjust my budget (personal and business)?

Ideally, both personal and business budgets should be reviewed and adjusted at least monthly. More frequent reviews (weekly or bi-weekly) might be necessary during periods of significant change or uncertainty.