How to Process Payroll Manually unveils the intricacies of managing employee compensation without relying on automated systems. This guide delves into the fundamental components of payroll, from calculating gross and net pay to navigating tax deductions and ensuring legal compliance. We’ll explore various compensation models, address common payroll errors, and offer practical advice for maintaining accurate and secure payroll records, empowering you to confidently handle this crucial business function.

Mastering manual payroll processing requires attention to detail and a thorough understanding of relevant regulations. This comprehensive guide provides a step-by-step approach, equipping you with the knowledge and tools to accurately calculate wages, manage deductions, and distribute payments efficiently. We will cover essential topics such as gathering employee information, calculating taxes, preparing payroll documents, and maintaining meticulous records, all while emphasizing the importance of accuracy and legal compliance.

Understanding Payroll Fundamentals

Processing payroll manually requires a solid grasp of fundamental payroll concepts. Accurate calculations are crucial to ensure employees receive the correct compensation and the business remains compliant with tax regulations. This section will cover the key components of payroll and provide a framework for manual calculation.

Payroll Components

Payroll involves several key components. Understanding these is essential for accurate processing. Gross pay represents the total earnings before any deductions. Net pay, also known as take-home pay, is the amount an employee receives after all deductions have been subtracted from gross pay. Deductions encompass various items withheld from gross pay, including taxes (federal, state, local) and other pre-tax or post-tax deductions such as health insurance premiums, retirement contributions, or union dues. Taxes are mandatory deductions levied by government agencies at various levels.

Types of Employee Compensation

Employees may receive compensation in various forms. Salary refers to a fixed amount paid regularly, typically monthly or bi-weekly, regardless of the number of hours worked. Hourly pay is calculated based on the employee’s hourly rate multiplied by the number of hours worked. Commission is a payment based on a percentage of sales or other performance metrics. Some employees may receive a combination of these compensation types, such as a base salary plus commission.

Calculating Gross Pay

Calculating gross pay varies depending on the compensation type.

Salary

For salaried employees, gross pay is straightforward. It’s simply the employee’s annual salary divided by the number of pay periods in a year. For example, an annual salary of $60,000 paid bi-weekly (26 pay periods) results in a gross pay of $2,307.69 per pay period ($60,000 / 26).

Hourly

For hourly employees, gross pay is calculated by multiplying the hourly rate by the number of hours worked. For instance, an employee earning $15 per hour and working 40 hours in a week earns a gross pay of $600 ($15/hour * 40 hours). Overtime pay, often at a rate of 1.5 times the regular rate, must be considered for hours exceeding a standard workweek (often 40 hours).

Commission

Commission-based gross pay depends on the sales or performance achieved. If an employee earns a 5% commission on sales and generates $10,000 in sales, their gross pay from commission is $500 ($10,000 * 0.05). Often, a base salary is combined with commission.

Sample Payroll Calculations

The following table illustrates sample calculations for gross pay, deductions, and net pay. These are simplified examples and do not include all potential deductions.

| Employee | Gross Pay | Deductions | Net Pay |

|---|---|---|---|

| John Doe (Salary) | $2,307.69 | $500 (Taxes & Insurance) | $1,807.69 |

| Jane Smith (Hourly) | $600 | $100 (Taxes) | $500 |

| Peter Jones (Commission) | $500 | $75 (Taxes) | $425 |

Calculating Deductions and Taxes

Accurately calculating and deducting taxes and other withholdings is crucial for compliant payroll processing. This section details the various types of deductions, both mandatory and voluntary, and Artikels the calculation process for federal income tax withholding, along with state and local tax considerations. Understanding these calculations ensures employees receive their net pay accurately and the business remains compliant with tax regulations.

Mandatory Deductions: Federal, State, and Local Taxes

Mandatory deductions represent legally required withholdings from an employee’s gross pay. These primarily consist of federal, state, and sometimes local income taxes. The amounts withheld depend on factors such as the employee’s filing status, claimed allowances, and income level. Federal income tax withholding is governed by IRS guidelines, while state and local tax rates and calculation methods vary by jurisdiction.

Voluntary Deductions: Employee Choices

Employees often elect voluntary deductions from their gross pay for various purposes. Common examples include health insurance premiums, retirement plan contributions (such as 401(k) plans), and payments towards other benefits or debt repayments (like student loans). These deductions reduce the employee’s taxable income and net pay, reflecting their personal financial choices. Employers typically facilitate these deductions by processing them alongside mandatory withholdings.

Federal Income Tax Withholding Calculation

The IRS provides various methods for calculating federal income tax withholding, including wage bracket tables and the percentage method. The wage bracket method uses pre-calculated tables based on an employee’s wages, filing status, and allowances. The percentage method requires more complex calculations using tax rates and taxable income. For example, using the percentage method, an employee’s taxable income is determined by subtracting allowances from their gross pay. This taxable income is then applied to the applicable tax brackets to determine the tax liability. The IRS Publication 15 (Circular E) provides detailed instructions and tables for accurate calculation.

State and Local Tax Calculation

State and local income tax calculations mirror the federal process, albeit with varying rates and brackets. Each state and locality has its own tax laws, rates, and forms. For instance, a state might have a progressive tax system with different rates for different income levels. An employee earning $50,000 annually might pay a lower tax rate on the first $20,000 than on the remaining $30,000. Similarly, local taxes, where applicable, add another layer of deduction, calculated according to the specific local tax codes. Accurate calculation requires consulting the relevant state and local tax guidelines. Many states provide online tax calculators or resources to simplify the process.

Preparing Payroll Documents

Creating and maintaining accurate payroll documents is crucial for both efficient payroll processing and legal compliance. These documents serve as a record of employee compensation, deductions, and net pay, providing essential information for tax filings and audits. Properly organized documents streamline the entire payroll process and minimize the risk of errors.

A well-structured payroll system relies on meticulously maintained records. This includes not only the final payroll register but also supporting documentation such as time sheets, benefit enrollment forms, and tax withholding information. The accuracy of these documents directly impacts the accuracy of the payroll calculations and the subsequent tax filings.

Payroll Register Design

A payroll register is a summary of all employee payments for a specific pay period. It’s a vital document for tracking payroll data and ensuring accuracy. The following table illustrates a sample payroll register design, adaptable to your specific needs. Remember to tailor it to reflect your company’s specific deductions and benefits.

| Employee Name | Employee ID | Gross Pay | Net Pay |

|---|---|---|---|

| John Doe | 12345 | $2000 | $1500 |

| Jane Smith | 67890 | $2500 | $1900 |

| Peter Jones | 13579 | $1800 | $1350 |

Best Practices for Accurate Payroll Records

Maintaining accurate payroll records requires consistent attention to detail and adherence to established procedures. These practices help prevent errors and ensure legal compliance.

- Use a standardized format: Employ a consistent format for all payroll documents to ensure clarity and easy data entry. This includes using the same format for time sheets, payroll registers, and other relevant documents.

- Regularly review and reconcile: Periodically review all payroll documents to identify and correct any discrepancies. Reconcile payroll data with bank statements and other financial records to ensure accuracy.

- Implement a system of checks and balances: Establish a system where multiple individuals review and approve payroll documents before processing payments. This helps to identify and prevent errors.

- Maintain secure storage: Store all payroll records securely, both physically and electronically. Implement appropriate access controls to protect sensitive employee data.

- Regularly back up data: Regularly back up all payroll data to prevent data loss in case of system failure or other unforeseen events.

Legal Compliance and Payroll Records

Maintaining accurate and complete payroll records is not merely a matter of good business practice; it’s a legal requirement. These records are essential for complying with various labor laws and tax regulations. Failure to maintain proper records can result in significant penalties and legal ramifications.

Accurate records are crucial for demonstrating compliance with minimum wage laws, overtime regulations, and other employment standards. They also provide essential information for tax filings, including income tax withholding, social security tax, and unemployment insurance contributions. Proper record-keeping helps protect both the employer and the employee from potential disputes and ensures smooth audits by relevant authorities.

Maintaining accurate payroll records is crucial for legal compliance and minimizing the risk of penalties.

Distributing Payroll Payments

Distributing payroll payments accurately and efficiently is a crucial final step in the payroll process. Choosing the right method depends on factors like employee preference, company size, and budget. This section Artikels the most common methods and provides guidance on their implementation.

Two primary methods exist for distributing payroll payments: payroll checks and direct deposit. Each has its own advantages and disadvantages, which will be explored in detail below.

Payroll Check Distribution

Preparing and distributing payroll checks involves several steps to ensure accuracy and compliance. Errors can lead to delays, employee dissatisfaction, and potential legal issues. Therefore, meticulous attention to detail is paramount.

A step-by-step guide for preparing payroll checks is provided below:

- Verify the employee’s net pay, ensuring all deductions and taxes have been correctly calculated.

- Write the check amount in both numerals and words. Ensure consistency between the two.

- Fill in the date and the employee’s name and address accurately. Double-check spelling.

- Sign the check. Only authorized personnel should sign payroll checks.

- Record the check number and amount in the payroll register.

- Distribute checks securely, often via internal mail or hand delivery, ensuring appropriate security measures are in place to prevent theft or loss.

Direct Deposit Setup

Direct deposit is an increasingly popular method for payroll distribution due to its convenience and efficiency. Setting up direct deposit requires obtaining the necessary banking information from employees and ensuring its accuracy. This information must be handled securely and confidentially.

The process for setting up direct deposit typically involves the following steps:

- Provide employees with a direct deposit authorization form. This form should clearly request the employee’s bank name, account number, and routing number. It should also include a statement regarding the employee’s consent and the employer’s data security policy.

- Verify the accuracy of the provided banking information. Incorrect information can lead to payment delays or non-delivery of funds.

- Input the banking details into the payroll system. This typically involves entering the account and routing numbers.

- Test the direct deposit process before implementing it company-wide to identify and rectify any potential issues early.

- Ensure compliance with relevant regulations concerning employee data privacy and security.

Comparison of Payment Methods

Both payroll checks and direct deposit offer distinct advantages and disadvantages. A careful consideration of these factors is crucial when selecting a payment method.

| Feature | Payroll Checks | Direct Deposit |

|---|---|---|

| Cost | Higher due to check printing, postage, and handling. | Lower, potentially eliminating check printing and mailing costs. |

| Convenience | Less convenient for employees; requires physical retrieval of checks. | More convenient for employees; funds are automatically deposited into their accounts. |

| Security | Greater risk of loss or theft. | More secure; reduces the risk of lost or stolen checks. |

| Efficiency | Less efficient; involves manual processing and distribution. | More efficient; automated processing and distribution. |

| Employee Preference | May be preferred by some employees, particularly those without bank accounts. | Generally preferred by most employees due to convenience and security. |

Maintaining Payroll Records

Maintaining accurate and organized payroll records is crucial for legal compliance, efficient auditing, and the smooth operation of your business. These records serve as a verifiable history of employee compensation, tax withholdings, and other relevant financial data. Proper record-keeping protects both the employer and the employee, ensuring accurate payment and preventing potential disputes.

Essential Payroll Documents for Compliance and Auditing

Maintaining comprehensive payroll records involves keeping several key documents. These documents are essential for demonstrating compliance with labor laws, tax regulations, and for facilitating smooth audits. Failure to maintain these records adequately can result in penalties and legal repercussions.

- Employee Records: These include applications, contracts, W-4 forms (for tax withholding), I-9 forms (verifying employment eligibility), and any other relevant agreements or documentation.

- Payroll Registers: A detailed record of each employee’s gross pay, deductions, and net pay for each pay period. This is a central document for tracking all payroll transactions.

- Tax Forms: This includes copies of all filed tax returns (e.g., 941, W-2, 1099), supporting documentation for tax calculations, and records of payments made to relevant tax authorities.

- Payment Records: Proof of payment to employees, whether by check, direct deposit, or other methods. This might include bank statements, payment logs, or canceled checks.

- Timekeeping Records: Detailed records of employee hours worked, including overtime, sick leave, and vacation time. This documentation is crucial for accurate calculation of wages.

Best Practices for Organizing and Storing Payroll Records

Effective organization and storage of payroll records are paramount for easy access and retrieval. A well-structured system simplifies audits and reduces the risk of errors or data loss.

A recommended approach is to use a combination of physical and digital filing systems. Physical files should be stored in a secure, climate-controlled environment, preferably in fireproof cabinets. Digital records should be stored on a secure server with appropriate access controls and regular backups. Consider using a cloud-based solution for enhanced security and accessibility.

A clear and consistent filing system is essential. This might involve organizing documents by employee name, pay period, or tax year. A detailed indexing system, either manual or digital, will further enhance the searchability of your records.

Data Security and Confidentiality in Payroll Record Keeping

Payroll data is highly sensitive and confidential. Protecting this information is crucial for maintaining employee trust and complying with data privacy regulations.

Implement robust security measures to prevent unauthorized access, use, or disclosure of payroll data. This includes password-protected computer systems, secure file storage, and encryption of sensitive data. Limit access to payroll records to authorized personnel only, and regularly review and update security protocols. Employee training on data security best practices is also vital.

Compliance with regulations such as the Fair Credit Reporting Act (FCRA) and other relevant privacy laws is essential. These regulations dictate how sensitive employee data must be handled and protected.

Sample Payroll Document Filing System

A well-structured filing system is essential for efficient management of payroll documents. Here’s an example:

Main Folders:

- Employee Files (alphabetical by last name)

- Payroll Registers (by year and pay period)

- Tax Documents (by year and tax form)

- Payment Records (by year and pay period)

- Timekeeping Records (by year and employee)

Subfolders within Employee Files:

- Application

- Contract

- W-4

- I-9

- Pay Stubs

- Performance Reviews

This system allows for easy retrieval of specific documents, ensuring efficient management of payroll data. Adapt this structure to fit your specific needs and business size.

Do not overlook the opportunity to discover more about the subject of Best Bookkeeping Software for Small Businesses.

Common Payroll Errors and How to Avoid Them: How To Process Payroll Manually

Manual payroll processing, while offering a degree of control, increases the risk of errors. Accuracy is paramount to maintain employee morale and avoid legal complications. Understanding common mistakes and implementing preventative measures is crucial for smooth payroll operations.

Incorrect Wage Calculations, How to Process Payroll Manually

Inaccurate wage calculations stem from various sources, including misinterpretations of hourly rates, overtime calculations, or incorrect application of bonuses and commissions. For instance, failing to properly calculate overtime pay at 1.5 times the regular rate for hours exceeding 40 in a workweek, as mandated by many jurisdictions, is a frequent error. Similarly, miscalculating commission structures or forgetting to include bonuses can lead to underpayment.

- Solution: Develop a clear and detailed pay calculation sheet that includes all relevant pay components. Double-check all calculations, preferably using a calculator or spreadsheet software to minimize manual calculation errors. Ensure a thorough understanding of all applicable wage and hour laws and regulations.

- Preventative Measures: Implement a system of checks and balances, perhaps involving a second person reviewing calculations before finalizing payroll. Regularly update pay rates and commission structures to reflect any changes.

- Consequences: Underpayment can lead to employee dissatisfaction, legal action, and reputational damage. Overpayment may strain the company’s finances.

Deduction Errors

Errors in calculating and deducting taxes and other deductions (e.g., health insurance, retirement contributions) are common. These errors often result from using incorrect tax tables, applying incorrect deduction rates, or simply making mathematical mistakes. For example, using an outdated tax bracket or incorrectly applying a dependent’s exemption can lead to significant discrepancies.

- Solution: Always use the most up-to-date tax tables and deduction information from official sources. Employ software or spreadsheets to automate calculations and reduce manual error. Carefully review each employee’s deduction information to ensure accuracy.

- Preventative Measures: Regularly update tax withholding information. Implement a system for verifying employee deduction elections against their payroll records. Conduct regular training for payroll personnel on relevant tax laws and regulations.

- Consequences: Incorrect deductions can result in penalties from tax authorities, employee complaints, and potential legal action. It can also damage employee trust and create administrative headaches.

Data Entry Mistakes

Simple data entry errors, such as typos in employee names or Social Security numbers, or incorrect hours worked, are surprisingly frequent. These seemingly minor mistakes can have significant downstream consequences. For instance, a wrong Social Security number could delay tax filings and cause complications with government agencies.

- Solution: Double-check all data entries. Use data validation tools in spreadsheets to minimize the entry of incorrect data. Implement a system for verifying data accuracy before processing payroll.

- Preventative Measures: Use standardized data entry forms. Train employees on proper data entry procedures. Implement regular data audits to identify and correct errors.

- Consequences: Data entry errors can lead to delays in payments, incorrect tax filings, and difficulty in tracking payroll information. They can also cause significant frustration for both employees and payroll administrators.

Failure to Update Payroll Records

Failing to update employee information, such as changes in pay rates, addresses, or withholding information, can lead to significant errors. For example, not updating an employee’s address may result in paychecks being sent to the wrong location.

- Solution: Establish a system for regularly updating employee information. Implement a process for employees to notify payroll of any changes. Conduct regular audits to ensure records are up-to-date.

- Preventative Measures: Use a centralized system for storing employee information. Require employees to submit updated information in writing or through a secure online portal.

- Consequences: Outdated information can result in incorrect payments, delayed payments, and legal complications.

Illustrative Example

This section provides a detailed manual payroll calculation for two hypothetical employees, showcasing different compensation types and deduction levels. Understanding this example will solidify your grasp of the manual payroll process. We will walk through each step, from calculating gross pay to generating net pay.

Employee 1: Hourly Employee

Employee 1, Sarah Jones, is an hourly employee earning $15 per hour. She worked 40 regular hours and 5 overtime hours (at 1.5 times her regular rate) during the pay period. Her federal tax withholding is 15%, state tax withholding is 5%, and she contributes 5% to her 401k.

Step 1: Calculate Gross Pay

Regular Pay: 40 hours * $15/hour = $600

Overtime Pay: 5 hours * ($15/hour * 1.5) = $112.50

Gross Pay: $600 + $112.50 = $712.50

Step 2: Calculate Deductions

Federal Tax: $712.50 * 0.15 = $106.88

State Tax: $712.50 * 0.05 = $35.63

401k Contribution: $712.50 * 0.05 = $35.63

Step 3: Calculate Net Pay

Total Deductions: $106.88 + $35.63 + $35.63 = $178.14

Net Pay: $712.50 – $178.14 = $534.36

Employee 2: Salaried Employee

Employee 2, John Smith, is a salaried employee with a monthly salary of $4,000. His federal tax withholding is 20%, state tax withholding is 7%, and he contributes 10% to his health savings account (HSA).

Step 1: Calculate Gross Pay

Gross Pay: $4000

Step 2: Calculate Deductions

Federal Tax: $4000 * 0.20 = $800

State Tax: $4000 * 0.07 = $280

HSA Contribution: $4000 * 0.10 = $400

Step 3: Calculate Net Pay

Total Deductions: $800 + $280 + $400 = $1480

Net Pay: $4000 – $1480 = $2520

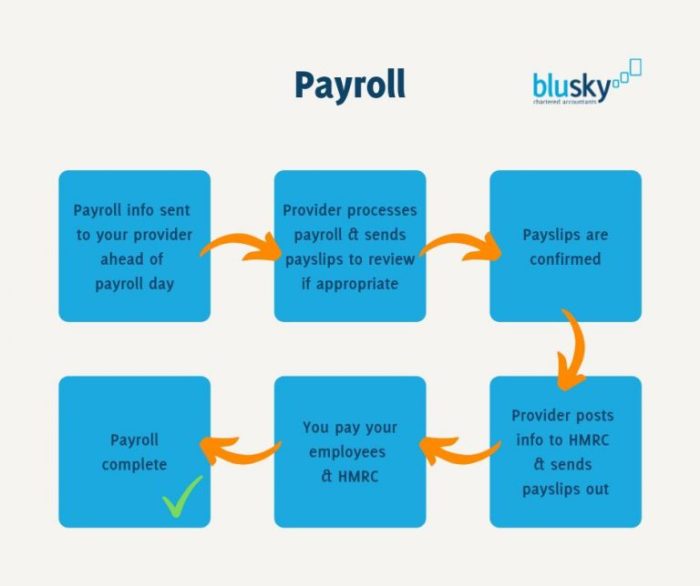

Process Flow Visualization

Imagine a flowchart. The process begins with gathering employee information (hours worked, salary, etc.). This feeds into the gross pay calculation block, which branches out based on whether the employee is hourly or salaried. For hourly employees, overtime calculations are included. Next, the deductions block calculates taxes and other withholdings. Finally, the net pay is calculated by subtracting total deductions from gross pay. The final output is the employee’s paycheck information. This visual representation clearly illustrates the sequential nature of the manual payroll process.

Final Thoughts

Successfully processing payroll manually requires precision and adherence to regulations. By understanding the fundamental principles of payroll calculation, employing effective record-keeping practices, and proactively addressing potential errors, you can confidently manage your company’s compensation process. This guide provides a solid foundation for efficient and compliant manual payroll management, enabling you to focus on other crucial aspects of your business operations. Remember to always consult with relevant tax and legal professionals for specific guidance related to your location and circumstances.

Questions Often Asked

What are the potential legal consequences of payroll errors?

Payroll errors can lead to penalties, fines, legal action from employees or government agencies, and reputational damage.

How often should payroll be processed?

Payroll frequency varies; common schedules include weekly, bi-weekly, semi-monthly, and monthly. The chosen frequency should align with company policy and employee agreements.

What software can assist with manual payroll calculations, even if not fully automating the process?

Spreadsheet software like Microsoft Excel or Google Sheets can be used to organize data and perform calculations, aiding in the manual payroll process.

How do I handle employee terminations in a manual payroll system?

Ensure final paychecks accurately reflect all earned wages, accrued vacation time, and any other applicable payments. Maintain detailed records of the termination process for compliance.