Cash Flow Statement Explained for Beginners: Understanding a company’s cash flow is crucial for assessing its financial health and making informed business decisions. This guide provides a clear and concise explanation of cash flow statements, demystifying the complexities for those new to financial analysis. We will explore the three main sections – operating, investing, and financing activities – and illustrate how to interpret this vital financial statement.

We’ll use real-world examples and simple explanations to make the concepts accessible, covering everything from calculating net cash flow to understanding how cash flow impacts a company’s long-term growth and strategic planning. Whether you’re a student, entrepreneur, or simply curious about finance, this guide will equip you with the foundational knowledge necessary to confidently navigate the world of cash flow statements.

Introduction to Cash Flow Statements: Cash Flow Statement Explained For Beginners

Understanding how much money a business actually has on hand, and how that money moves, is crucial for its success. This is where the cash flow statement comes in. It’s a financial statement that provides a clear picture of the cash inflows (money coming in) and outflows (money going out) of a business over a specific period. Unlike other financial statements that focus on accrual accounting (recording revenue when earned, regardless of when cash is received), the cash flow statement solely focuses on actual cash transactions.

The purpose of a cash flow statement is to show how a company generates and uses its cash. It’s a vital tool for assessing a company’s liquidity (ability to meet short-term obligations), solvency (ability to meet long-term obligations), and overall financial health. By analyzing cash flow, investors, creditors, and managers can make informed decisions about the company’s future.

A Real-World Analogy

Imagine you’re running a lemonade stand. You receive cash from selling lemonade (cash inflow). You spend cash on lemons, sugar, and cups (cash outflow). Your cash flow statement would show the difference between the money you earned and the money you spent. A positive cash flow means you have more cash coming in than going out, while a negative cash flow indicates the opposite. This simple example illustrates the core concept of tracking cash movements, which is fundamental to understanding a business’s financial well-being. Just like tracking your lemonade stand’s cash, larger businesses need to meticulously track their cash flow to ensure they remain solvent and profitable.

The Evolution of Cash Flow Statements

While the formal structure of cash flow statements as we know them today emerged later, the underlying concept of tracking cash has been integral to accounting practices for centuries. Early merchants and traders kept meticulous records of their cash transactions to manage their businesses effectively. The formalization of accounting standards in the 20th century led to the development of standardized formats for presenting cash flow information. The increasing complexity of business operations and the need for more transparent financial reporting further refined the structure and reporting requirements of cash flow statements. International accounting standards, such as those issued by the IASB (International Accounting Standards Board), now mandate the preparation and presentation of cash flow statements for publicly traded companies, ensuring consistency and comparability across different jurisdictions. The evolution reflects a growing recognition of the critical role cash flow plays in assessing a company’s financial performance and stability.

The Three Main Sections of a Cash Flow Statement

The cash flow statement provides a comprehensive overview of how a company’s cash balance changes over a period. Understanding its three main sections is crucial to interpreting a company’s financial health and liquidity. These sections categorize cash inflows (money coming in) and outflows (money going out) into distinct business activities.

Operating Activities

This section focuses on cash flows resulting from the company’s core business operations. It reflects the cash generated or used from selling goods or services, paying suppliers, and covering operating expenses. A positive cash flow from operating activities generally indicates a healthy and profitable business. However, it’s important to remember that a positive operating cash flow doesn’t necessarily mean a company is highly profitable; it simply means they are effectively managing their cash flow from daily operations.

Investing Activities

The investing activities section details cash flows related to long-term assets. These assets are typically used to generate future income, and examples include property, plant, and equipment (PP&E), investments in other companies, and acquisitions. Cash outflows in this section represent purchases of these assets, while inflows reflect the sale of such assets. A significant outflow often suggests a company is investing in its future growth, while inflows might signal a company is divesting from certain areas.

Financing Activities

This section tracks cash flows related to how a company finances its operations. This includes transactions with lenders and shareholders. Cash inflows here represent activities such as issuing debt (loans) or equity (selling shares), while outflows include debt repayments, dividend payments, and share repurchases. Analyzing this section helps understand a company’s capital structure and its reliance on debt or equity financing.

| Activity Type | Cash Inflow Example | Cash Outflow Example |

|---|---|---|

| Operating Activities | Cash received from customers for goods sold | Cash paid to suppliers for inventory |

| Investing Activities | Proceeds from the sale of equipment | Purchase of new machinery |

| Financing Activities | Proceeds from issuing bonds | Repayment of bank loan |

Understanding Cash Flow from Operating Activities

Operating activities represent the core business functions of a company. Understanding the cash flow generated from these activities is crucial for assessing a company’s profitability and liquidity. This section will delve into how to calculate net cash flow from operating activities using the direct and indirect methods, highlighting their differences and providing examples.

Net Cash Flow from Operating Activities Calculation Methods

The net cash flow from operating activities can be calculated using two primary methods: the direct method and the indirect method. Both methods ultimately aim to arrive at the same figure – the net cash generated or used by the company’s core operations. However, they approach this calculation differently.

Direct Method

The direct method calculates net cash flow from operating activities by directly adding up all cash inflows and subtracting all cash outflows related to operations. This involves reviewing actual cash receipts and payments. For example, cash received from customers for sales is a cash inflow, while cash paid to suppliers for inventory is a cash outflow. The direct method offers a clearer picture of the actual cash generated from operations. However, it is less commonly used because it requires detailed cash records for every transaction, making it more time-consuming and potentially more costly to implement.

Indirect Method

The indirect method starts with net income from the income statement and adjusts it to reflect cash flows. This involves adding back non-cash expenses (like depreciation and amortization) and adjusting for changes in working capital accounts (accounts receivable, accounts payable, inventory). For example, an increase in accounts receivable indicates that sales were made on credit and not yet converted to cash, thus reducing the cash flow. Conversely, an increase in accounts payable implies that expenses were incurred but not yet paid, increasing the cash flow. The indirect method is more commonly used because it leverages readily available information from the accounting records, making it more efficient. However, it can be less transparent in showing the actual cash inflows and outflows.

Comparison of Direct and Indirect Methods

| Feature | Direct Method | Indirect Method |

|---|---|---|

| Starting Point | Cash receipts and payments | Net income |

| Process | Direct summation of cash inflows and outflows | Adjustments to net income |

| Transparency | Highly transparent | Less transparent |

| Complexity | More complex and time-consuming | Less complex and time-saving |

| Common Usage | Less common | More common |

Examples of Transactions Affecting Operating Cash Flow

Several transactions directly impact operating cash flow. These can be categorized as either increasing or decreasing the net cash flow from operating activities.

Transactions Increasing Operating Cash Flow

- Cash received from customers for goods or services sold.

- Interest received on investments.

- Dividends received from investments (if considered operating activities).

- Decrease in accounts receivable (customers paying outstanding balances).

- Increase in accounts payable (delaying payments to suppliers).

Transactions Decreasing Operating Cash Flow

- Cash paid to suppliers for goods or services purchased.

- Cash paid for salaries and wages.

- Cash paid for rent and utilities.

- Cash paid for interest expense.

- Increase in accounts receivable (selling goods on credit).

- Decrease in accounts payable (paying outstanding balances to suppliers).

Understanding Cash Flow from Investing Activities

The investing activities section of the cash flow statement shows how a company uses its cash to acquire and dispose of long-term assets. Unlike operating activities, which focus on the day-to-day business, investing activities reflect strategic decisions impacting the company’s future growth and profitability. Understanding this section provides crucial insights into a company’s investment strategy and its potential for long-term success.

Investing activities primarily involve the purchase and sale of long-term assets. These assets are generally expected to provide economic benefits for more than one year. This section reveals how a company is allocating capital to expand its operations, upgrade its technology, or acquire other businesses. A positive cash flow in this section generally indicates that the company is selling more assets than it is buying, while a negative cash flow suggests the opposite.

Capital Expenditures and Acquisitions

Capital expenditures (CapEx) represent investments in fixed assets such as property, plant, and equipment (PP&E). Acquisitions involve purchasing other companies or significant portions of their operations. Both CapEx and acquisitions are significant cash outflows, reflecting substantial investments in the company’s future. For example, a manufacturing company might invest in new machinery (CapEx) to increase production capacity, while a technology firm might acquire a smaller competitor (Acquisition) to expand its market share. These are usually significant expenses shown as negative cash flows in this section of the statement. The sale of such assets would, conversely, result in a positive cash flow.

Examples of Investing Activities Increasing and Decreasing Cash Flow

Several transactions impact the investing activities section. The purchase of equipment, buildings, or land decreases cash flow, while the sale of these assets increases cash flow. Similarly, investing in securities (like stocks and bonds) decreases cash flow initially, while their subsequent sale increases cash flow. Acquiring another company is a substantial cash outflow, while divesting from a subsidiary represents a cash inflow. For instance, if a company sells a piece of land it owned for $1 million, this would be recorded as a positive cash flow from investing activities. Conversely, if the company purchases a new factory for $10 million, it would be a negative cash flow.

Impact of Investing Activities on Long-Term Growth

Investing activities significantly influence a company’s long-term growth trajectory. Strategic investments in CapEx and acquisitions can enhance operational efficiency, expand market reach, and ultimately drive profitability. Consider these points:

- Increased Production Capacity: Investing in new equipment or facilities can boost production output, leading to higher sales and revenue.

- Technological Advancement: Investments in research and development or acquiring companies with cutting-edge technology can provide a competitive advantage.

- Market Expansion: Acquisitions can rapidly expand a company’s market presence and customer base.

- Diversification: Investing in diverse business areas reduces risk and creates new revenue streams.

- Improved Efficiency: Investments in automation or process improvements can lower operating costs and increase profitability.

Understanding Cash Flow from Financing Activities

The cash flow from financing activities section of a cash flow statement shows how a company raises and repays capital. This includes transactions with lenders, investors, and other creditors. Understanding this section provides crucial insight into a company’s capital structure and its ability to manage its long-term debt and equity. It reveals how the company funds its operations and growth, impacting its financial health and sustainability.

Financing activities primarily involve transactions that alter a company’s capital structure. These transactions directly affect the long-term funding of the business. They differ significantly from operating activities, which focus on the day-to-day running of the business, and investing activities, which relate to acquiring and disposing of long-term assets.

Debt Financing and Equity Financing

Debt financing involves borrowing money, increasing liabilities. This can be through loans from banks, issuing bonds, or other forms of debt instruments. Equity financing, conversely, involves selling ownership stakes in the company, increasing equity. This is typically achieved by issuing new shares of stock. Both methods have different implications for a company’s financial position and risk profile. Debt financing increases financial leverage, while equity financing dilutes ownership but reduces financial risk.

The Impact of Dividends Paid on Cash Flow, Cash Flow Statement Explained for Beginners

Dividends paid represent a cash outflow from financing activities. When a company distributes dividends to its shareholders, it reduces its cash reserves. The amount of dividends paid is determined by the company’s board of directors and depends on factors like profitability, cash flow, and future investment needs. Significant dividend payments can significantly impact a company’s cash position, especially for companies with limited cash reserves. Companies may choose to reduce or suspend dividends during periods of financial difficulty or when prioritizing reinvestment in the business.

Effects of Various Financing Activities on Cash Flow

The following list summarizes the impact of various financing activities on cash flow. Note that these are generally presented as negative (cash outflow) or positive (cash inflow) values on the statement.

- Issuance of Debt (e.g., loans, bonds): This results in a cash inflow, as the company receives funds from lenders.

- Issuance of Stock (e.g., common stock, preferred stock): This also results in a cash inflow, as the company receives funds from investors in exchange for ownership.

- Repayment of Debt (e.g., loan principal, bond redemption): This represents a cash outflow, as the company uses its cash to repay its obligations.

- Repurchase of Stock (e.g., buybacks): This is a cash outflow, as the company uses its cash to acquire its own shares.

- Payment of Dividends: This is a cash outflow, as the company distributes cash to its shareholders.

Analyzing a Cash Flow Statement

Interpreting a cash flow statement is crucial for understanding a company’s financial health, particularly its ability to meet its short-term and long-term obligations. It provides a dynamic view of how cash moves in and out of the business, offering insights that are not readily apparent from the static picture presented by the balance sheet or the accrual-based income statement. By analyzing the statement’s three main sections – operating, investing, and financing activities – a comprehensive assessment of liquidity and financial stability can be achieved.

Analyzing a company’s cash flow statement involves a thorough examination of its cash inflows and outflows. This process helps determine the company’s liquidity, solvency, and overall financial health. Effective analysis necessitates a comparative approach, often involving trend analysis over multiple periods and benchmarking against industry peers. This allows for the identification of both positive and negative trends, providing valuable insights for decision-making.

Assessing Liquidity with Cash Flow Data

A company’s liquidity, its ability to meet its short-term obligations, is directly reflected in its cash flow statement. Specifically, the cash flow from operating activities section is paramount. A consistently positive cash flow from operations indicates a healthy ability to generate cash from core business activities, suggesting strong liquidity. Conversely, consistently negative operating cash flow raises serious concerns about the company’s ability to pay its bills and sustain operations. For example, a company with high profits on its income statement but consistently negative operating cash flow might be facing challenges related to accounts receivable (customers not paying on time) or inventory management (holding excessive unsold inventory). Analyzing the relationship between net income and cash flow from operations helps identify discrepancies that may signal underlying problems. A significant difference between these two figures often requires further investigation.

Cash Flow Analysis in Conjunction with Other Financial Statements

The cash flow statement doesn’t exist in isolation; its true value is revealed when analyzed alongside the income statement and balance sheet. The income statement provides a picture of profitability using accrual accounting, which means it includes revenues and expenses regardless of when cash is actually received or paid. The balance sheet provides a snapshot of the company’s assets, liabilities, and equity at a specific point in time. By comparing the cash flow statement with these other statements, a more holistic understanding of the company’s financial position emerges. For instance, a company may report high profits on its income statement but show low or negative cash flow from operations, indicating potential issues with receivables collection or inventory turnover. This discrepancy highlights the limitations of relying solely on the income statement for assessing financial health. Similarly, changes in the balance sheet items, such as increases in accounts receivable or inventory, can be reconciled with cash flow data to understand the impact on cash balances.

Identifying Potential Financial Problems Using Cash Flow Data

Analyzing cash flow data can reveal various potential financial problems. For example, consistently declining cash flow from operations, even with increasing sales, might indicate pricing pressures or rising operating costs. A significant reliance on financing activities to fund operations – consistently high cash flow from financing activities compensating for negative operating cash flow – signals a potentially unsustainable business model. Furthermore, a substantial decrease in cash and cash equivalents over time, combined with negative operating cash flow, points towards an impending liquidity crisis. A real-world example would be a retail company that experiences strong sales growth but struggles to convert those sales into cash due to high credit sales and slow collection of receivables. This scenario would manifest as positive net income but negative cash flow from operations, ultimately threatening the company’s short-term solvency. Another example would be a company that consistently invests heavily in property, plant, and equipment (PP&E) resulting in negative free cash flow; this could indicate over-investment or inefficient capital allocation.

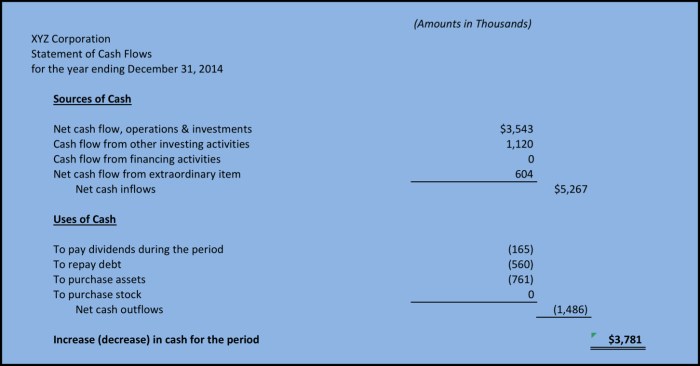

Illustrative Example: A Simple Cash Flow Statement

Let’s illustrate the concept of a cash flow statement with a hypothetical example of “The Daily Grind,” a small coffee shop. This example will demonstrate how various transactions affect the different sections of the statement.

The Daily Grind Coffee Shop: Cash Flow Statement for the Month of October

This statement summarizes The Daily Grind’s cash inflows and outflows for October. We’ll break down each transaction to understand its impact.

| Cash Flow Activity | Transaction | Amount ($) |

|---|---|---|

| Operating Activities | Cash sales from coffee and pastries | 15,000 |

| Operating Activities | Payment received from online orders | 2,000 |

| Operating Activities | Payment to suppliers (coffee beans, pastries) | -6,000 |

| Operating Activities | Salaries paid to employees | -4,000 |

| Operating Activities | Rent expense paid | -1,500 |

| Operating Activities | Utilities expense paid | -500 |

| Investing Activities | Purchase of new coffee machine | -3,000 |

| Investing Activities | Sale of old espresso machine | 500 |

| Financing Activities | Loan received from bank | 10,000 |

| Financing Activities | Loan repayment | -2,000 |

| Net Cash Flow | 6,500 |

Analysis of The Daily Grind’s Cash Flow

The Daily Grind generated a net positive cash flow of $6,500 in October. This indicates that the business generated more cash than it spent during the month. The strong cash flow from operating activities ($5,000; $17,000 inflow – $12,000 outflow) demonstrates profitability and efficient management of day-to-day operations. The investing activities resulted in a net outflow of $2,500, primarily due to the purchase of a new coffee machine. This is a capital expenditure aimed at improving efficiency and future profitability. Financing activities showed a net inflow of $8,000, largely due to the new loan received. The loan repayment is a regular expense associated with the financing of the business. Overall, The Daily Grind’s financial health appears to be positive, showing a capacity to generate profits and invest in its future. However, continued monitoring of cash flow is crucial for sustainable growth. A consistent positive cash flow is essential for the long-term success of the business.

Outcome Summary

Mastering the interpretation of cash flow statements empowers you to make well-informed decisions regarding business investments, expansion strategies, and overall financial health. By understanding the interplay between operating, investing, and financing activities, you gain valuable insights into a company’s liquidity, profitability, and long-term sustainability. Remember, a robust understanding of cash flow is not just for accountants; it’s a critical skill for anyone involved in the financial aspects of a business, large or small.

Helpful Answers

What is the difference between cash flow and profit?

Profit (net income) is an accounting measure that includes non-cash items like depreciation. Cash flow, on the other hand, focuses solely on the actual cash inflows and outflows during a specific period.

Why is analyzing cash flow important for investors?

Analyzing cash flow helps investors assess a company’s ability to meet its short-term obligations, fund future growth, and generate returns. It provides a more realistic picture of a company’s financial health than profit alone.

Can a company be profitable but still have negative cash flow?

Yes. This can happen if a company has high accounts receivable (customers haven’t paid yet) or makes significant capital expenditures (investments in long-term assets).

How often are cash flow statements prepared?

Cash flow statements are typically prepared quarterly and annually, mirroring the frequency of other financial statements.

Obtain a comprehensive document about the application of Tax Filing Deadlines for Small Businesses in 2025 that is effective.