Accounting for Inventory: FIFO vs LIFO Explained – Understanding how businesses account for their inventory is crucial for accurate financial reporting. This involves choosing a method for valuing inventory, with two prominent approaches being First-In, First-Out (FIFO) and Last-In, First-Out (LIFO). These methods significantly impact a company’s reported profits, taxes, and overall financial picture, particularly during periods of inflation or deflation. This exploration delves into the nuances of each method, highlighting their implications and helping you understand which might be most suitable for different business contexts.

We will examine the core principles of FIFO and LIFO, illustrating their effects on cost of goods sold and ending inventory. We’ll also compare and contrast their impact on key financial statements, exploring the advantages and disadvantages of each approach. Real-world examples will illuminate how these methods play out in various industries and economic climates, providing a practical understanding of their application.

Introduction to Inventory Accounting

Accurate inventory accounting is crucial for the financial health of any business, regardless of size or industry. Maintaining precise records ensures that a company has a clear understanding of its assets, allowing for informed decision-making regarding pricing, production, and overall business strategy. Inaccurate inventory data can lead to significant financial misstatements, impacting profitability, tax obligations, and investor confidence. This section will explore the fundamentals of inventory accounting, focusing on the definition, types, and financial statement implications of inventory valuation.

Inventory refers to the goods a company holds for the purpose of sale in the ordinary course of business. This includes raw materials, work-in-progress (WIP), and finished goods. The type of inventory held will vary depending on the nature of the business. A manufacturing company will likely have all three types, while a retail business will primarily hold finished goods. Accurate tracking of inventory levels is paramount to efficient operations and financial reporting.

Inventory Types

Inventory can be categorized in several ways, depending on the stage of production and intended use. Understanding these categories is vital for accurate accounting and analysis. Raw materials are the basic inputs used in the production process. Work-in-progress (WIP) represents goods that are partially completed but not yet ready for sale. Finished goods are completed products ready for sale to customers. The value assigned to each of these categories significantly influences the company’s financial statements.

Impact of Inventory Valuation on Financial Statements

The method used to value inventory directly affects the cost of goods sold (COGS) and the value of inventory reported on the balance sheet. This, in turn, impacts key financial metrics such as gross profit, net income, and current assets. Different valuation methods, such as FIFO (First-In, First-Out) and LIFO (Last-In, First-Out), will result in different COGS and ending inventory values, especially during periods of fluctuating prices. For example, during inflationary periods, LIFO will generally result in a higher COGS and lower net income compared to FIFO, due to the assumption that the most recently purchased (and therefore most expensive) goods are sold first. Conversely, during deflationary periods, LIFO will generally result in a lower COGS and higher net income compared to FIFO. The choice of inventory valuation method can have a significant impact on a company’s tax liability as well, as COGS is a deductible expense. The selection of an appropriate inventory valuation method is a crucial accounting decision that must be carefully considered based on the specific circumstances of the business.

FIFO (First-In, First-Out) Method

The First-In, First-Out (FIFO) method is an inventory valuation approach that assumes the oldest items in a company’s inventory are sold first. This aligns with the natural flow of goods in many businesses, where older products are prioritized for sale to avoid spoilage or obsolescence. The core principle of FIFO is that the cost of goods sold (COGS) reflects the cost of the oldest inventory items, while the ending inventory value represents the cost of the newest items.

This method’s simplicity and intuitive nature make it a popular choice across various industries.

Businesses Commonly Using FIFO

Many businesses find FIFO to be a practical inventory management method. Supermarkets, for example, often use FIFO to manage perishable goods like milk and produce. The oldest items are placed at the front of the shelves, ensuring they are sold before their expiration dates. Similarly, businesses selling seasonal items, such as clothing retailers selling winter coats, might employ FIFO to ensure that older stock is sold before the new season’s items arrive. Manufacturing companies with a continuous production process frequently use FIFO to track raw materials and finished goods.

FIFO’s Impact on Cost of Goods Sold and Ending Inventory During Inflation and Deflation

The impact of inflation and deflation on COGS and ending inventory is significant when using the FIFO method.

During periods of inflation (when prices are rising), FIFO results in a lower cost of goods sold and a higher value for ending inventory. This is because the older, cheaper items are expensed as COGS, while the newer, more expensive items remain in inventory. This can lead to higher reported profits in the short term, as COGS is lower, but also higher taxes.

Conversely, during periods of deflation (when prices are falling), FIFO results in a higher cost of goods sold and a lower value for ending inventory. The older, more expensive items are expensed as COGS, while the newer, cheaper items remain in inventory. This leads to lower reported profits in the short term, as COGS is higher.

| Scenario | Cost of Goods Sold (COGS) | Ending Inventory | Impact on Net Income |

|---|---|---|---|

| Inflation (Prices Rising) | Lower | Higher | Higher Net Income (potentially higher taxes) |

| Deflation (Prices Falling) | Higher | Lower | Lower Net Income (potentially lower taxes) |

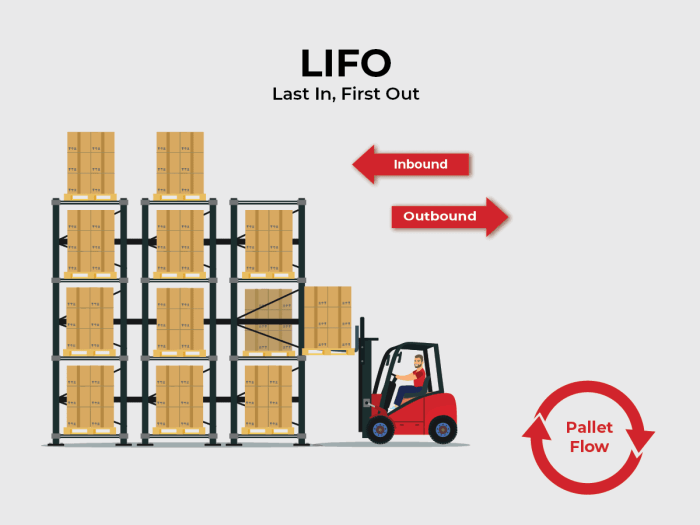

LIFO (Last-In, First-Out) Method: Accounting For Inventory: FIFO Vs LIFO Explained

The Last-In, First-Out (LIFO) method is an inventory costing method that assumes the most recently acquired items are the ones first sold. This contrasts sharply with FIFO, where the oldest items are assumed to be sold first. The core principle behind LIFO is that the cost of goods sold reflects the current market price of inventory.

LIFO operates on the assumption that the last units purchased are the first ones sold. This means that the cost of goods sold calculation uses the most recent purchase prices, while the value of ending inventory reflects the cost of the oldest units. This method is particularly useful in industries with rapidly changing prices, as it more accurately reflects the current economic reality in the cost of goods sold.

Industries Utilizing LIFO

LIFO is commonly used in industries where inventory is homogenous and easily interchangeable, such as those dealing with commodities like oil, gas, and metals. These industries often experience significant price fluctuations, and LIFO helps to more accurately reflect the impact of these fluctuations on profitability. Other industries that may use LIFO include manufacturing companies with large quantities of similar products and retailers selling fast-moving consumer goods where the assumption of last-in, first-out is a reasonable approximation of their actual inventory flow.

LIFO’s Impact on Cost of Goods Sold and Ending Inventory During Inflation and Deflation

During periods of inflation (rising prices), LIFO results in a higher cost of goods sold because the most expensive recent purchases are recorded as sold. This, in turn, leads to lower net income and lower tax liability. Conversely, the value of ending inventory will be lower under LIFO, as it is valued at the older, cheaper prices.

During periods of deflation (falling prices), LIFO results in a lower cost of goods sold because the least expensive, recent purchases are recorded as sold. This leads to higher net income and higher tax liability. Conversely, the value of ending inventory will be higher under LIFO, reflecting the more recent, lower prices.

For example, imagine a company that buys 10 units of a product at $10 each and later buys another 10 units at $12 each. Under LIFO, if they sell 15 units, the cost of goods sold would be calculated as (10 units x $12) + (5 units x $10) = $170. The value of the remaining 5 units in ending inventory would be $50 (5 units x $10). If prices had fallen to $8 and $10 instead, the cost of goods sold for the same 15 units would be (10 units x $10) + (5 units x $8) = $140.

Comparison of LIFO and FIFO Tax Implications

The choice between LIFO and FIFO has significant tax implications, especially during periods of inflation or deflation.

- Inflation: LIFO results in a higher cost of goods sold, leading to lower taxable income and lower tax liability. FIFO results in a lower cost of goods sold, leading to higher taxable income and higher tax liability.

- Deflation: LIFO results in a lower cost of goods sold, leading to higher taxable income and higher tax liability. FIFO results in a higher cost of goods sold, leading to lower taxable income and lower tax liability.

- Consistency: Once a company chooses a method (LIFO or FIFO), it must consistently apply it unless there is a justifiable reason to change. Changing methods requires specific accounting disclosures and may impact financial reporting.

Comparing FIFO and LIFO

Choosing between FIFO (First-In, First-Out) and LIFO (Last-In, First-Out) inventory costing methods significantly impacts a company’s financial statements. Understanding these effects is crucial for accurate financial reporting and decision-making. This section compares and contrasts the two methods, highlighting their influence on key financial metrics and outlining scenarios where one method might be preferred over the other.

Effects on Net Income, Taxes, and Financial Ratios

The primary difference between FIFO and LIFO lies in how they value cost of goods sold (COGS) and ending inventory. During periods of inflation, FIFO assumes that the oldest, and typically cheapest, inventory is sold first. This results in lower COGS, higher net income, and higher taxable income. Conversely, LIFO assumes that the newest, and typically most expensive, inventory is sold first. This leads to higher COGS, lower net income, and lower taxable income. This difference in net income directly affects various financial ratios. For instance, a higher net income under FIFO will lead to a higher return on assets (ROA) and profit margin compared to LIFO. Conversely, inventory turnover might appear higher under LIFO due to the higher COGS. During periods of deflation, the effects are reversed.

Circumstances Favoring FIFO or LIFO

The choice between FIFO and LIFO often depends on a company’s specific circumstances and goals. Companies operating in stable price environments might prefer FIFO for its simplicity and alignment with the actual physical flow of goods. The resulting higher net income can be advantageous for attracting investors and securing loans. However, in inflationary environments, LIFO’s lower net income can result in lower tax liabilities, a significant benefit for businesses seeking to minimize their tax burden. This lower tax burden can free up cash flow for reinvestment or other strategic initiatives. Furthermore, LIFO can be beneficial for companies whose inventory is perishable or quickly becomes obsolete, as it reflects the current market value of the goods sold more accurately.

Impact on Financial Statement Analysis

The choice of inventory costing method significantly impacts the interpretation of financial statements. Analysts need to be aware of the method used when comparing companies or analyzing trends over time. For example, a company using LIFO might show lower profitability compared to a competitor using FIFO, even if their operational efficiency is similar. This difference is solely due to the accounting method and not necessarily a reflection of underlying business performance. Consistent application of the chosen method is crucial for reliable financial reporting and meaningful comparisons.

| Feature | FIFO (First-In, First-Out) | LIFO (Last-In, First-Out) |

|---|---|---|

| Net Income | Higher during inflation, lower during deflation | Lower during inflation, higher during deflation |

| Taxes | Higher during inflation, lower during deflation | Lower during inflation, higher during deflation |

| Inventory Valuation | Reflects current market value of ending inventory during inflation | Reflects current market value of cost of goods sold during inflation |

| Advantages | Simple to understand and apply; reflects actual physical flow in many cases; higher net income can be attractive to investors | Lower taxes during inflation; better reflects current costs during inflation |

| Disadvantages | Higher taxes during inflation; may not reflect current market values during periods of rapid price changes | More complex to understand and apply; lower net income may be unattractive to investors; may not reflect actual physical flow |

Specific Inventory Scenarios

Understanding the practical application of FIFO and LIFO requires examining specific business scenarios. The optimal method depends heavily on the nature of the inventory and the business’s goals. Different inventory types and market conditions will lead to different financial statement outcomes under each method.

FIFO Scenario: A Grocery Store

Imagine a small grocery store specializing in fresh produce. They receive a shipment of 100 apples on Monday at $0.50 each, another 150 on Wednesday at $0.60 each, and a final 200 on Friday at $0.70 each. By Sunday, they’ve sold 300 apples. Using FIFO, the cost of goods sold (COGS) reflects the cost of the apples purchased first. Therefore, the COGS would be calculated as (100 apples * $0.50) + (150 apples * $0.60) + (50 apples * $0.70) = $160. The remaining inventory (150 apples) would be valued at (100 apples * $0.60) + (50 apples * $0.70) = $95. This accurately reflects the current market value of the remaining inventory, which is crucial for a business dealing with perishable goods. The income statement would show a higher gross profit due to the lower COGS, while the balance sheet would reflect a more realistic value for ending inventory.

LIFO Scenario: An Oil Refinery

Consider an oil refinery purchasing crude oil. They buy 1000 barrels on January 1st at $50/barrel, 1500 barrels on February 1st at $60/barrel, and 2000 barrels on March 1st at $70/barrel. During the first quarter, they refine and sell 3000 barrels. Using LIFO, the cost of goods sold is calculated using the most recently purchased inventory first. The COGS would be (2000 barrels * $70) + (1000 barrels * $60) = $200,000. The remaining inventory (1500 barrels) is valued at $50/barrel, or $75,000. This scenario showcases LIFO’s advantage in matching current costs with current revenues, particularly relevant in industries with fluctuating commodity prices. The income statement would show a lower gross profit (due to higher COGS) and a lower inventory valuation on the balance sheet, which reflects the older, potentially less valuable, inventory.

Impact of Inventory Obsolescence on FIFO and LIFO

Inventory obsolescence, where inventory becomes outdated or unsellable, significantly impacts both methods. With FIFO, older inventory is assumed to be sold first. If this older inventory becomes obsolete, the impact on COGS and net income is immediate, as its cost is recognized in the current period. LIFO, on the other hand, assumes the newest inventory is sold first. Therefore, the impact of obsolescence on COGS and net income is delayed until the older inventory is eventually sold or written off. However, the balance sheet will reflect the value of obsolete inventory under both methods, potentially leading to a need for write-downs, which negatively impacts net income in the period of the write-down. For example, if the grocery store from the FIFO example finds 50 of its oldest apples are rotten and unsaleable, the impact on the COGS and net income is immediate, whereas the oil refinery using LIFO might only see the impact when the older, less valuable inventory is eventually used or written off. This difference highlights the importance of considering inventory turnover rates and the risk of obsolescence when choosing between FIFO and LIFO.

Accounting Standards and Regulations

Inventory accounting methods, like FIFO and LIFO, are subject to strict accounting standards to ensure consistency and comparability across financial statements. These standards aim to provide a clear and accurate picture of a company’s financial health, facilitating informed decision-making by investors and stakeholders. The choice of method significantly impacts reported profits and asset values, making adherence to these rules crucial.

The primary accounting standards governing inventory accounting are Generally Accepted Accounting Principles (GAAP) in the United States and International Financial Reporting Standards (IFRS) internationally. Both frameworks provide guidelines on acceptable inventory costing methods, including FIFO and LIFO, but with key differences in their acceptance and application. Understanding these standards is essential for accurate financial reporting.

GAAP and IFRS Regulations on Inventory Accounting

GAAP allows for the use of both FIFO and LIFO, while IFRS permits only FIFO or the weighted-average cost method. This difference stems from differing philosophies; GAAP prioritizes the matching of current costs with current revenues (a benefit of LIFO), whereas IFRS emphasizes the reporting of inventory at the lower of cost or net realizable value, aligning better with FIFO’s approach. The choice of method under GAAP must be consistently applied from period to period, unless a change is justified and disclosed. Under IFRS, the selected method must be applied consistently, with changes requiring specific justification and disclosure. This consistency ensures reliable comparisons over time.

Limitations of FIFO and LIFO, Accounting for Inventory: FIFO vs LIFO Explained

FIFO, while generally preferred under IFRS, can lead to an overstatement of profits during periods of inflation, as older, lower-cost inventory is sold first. This can result in a higher tax liability. Conversely, LIFO, while permitted under GAAP, can lead to an understatement of profits during inflationary periods, as the higher cost of recent inventory is matched against current revenues. This can result in a lower tax liability, a key advantage for some businesses. Both methods also suffer from the limitation of not perfectly reflecting the actual flow of goods, which can be particularly relevant in industries with significant product obsolescence or spoilage. For example, a grocery store using FIFO might still experience losses from spoiled goods even though FIFO assumes the oldest goods are sold first.

Disclosure Requirements for Inventory Accounting Methods

Companies are required to clearly disclose the inventory accounting method used in their financial statements. This disclosure is typically found in the notes to the financial statements and provides essential context for understanding the reported figures. The disclosure should specify the method used (FIFO, LIFO, weighted-average cost, etc.) and explain any changes in method from previous periods. This transparency allows investors and analysts to accurately interpret the financial data and compare the company’s performance with others in the industry. Failure to disclose the inventory accounting method or any changes to it can lead to material misstatements in the financial statements and potentially attract regulatory scrutiny.

Impact on Financial Statement Analysis

The choice between FIFO and LIFO inventory costing methods significantly impacts a company’s financial statements, affecting how assets, liabilities, equity, revenues, and expenses are reported. These differences stem from how each method values the cost of goods sold (COGS) and the ending inventory. Understanding these impacts is crucial for accurate financial statement analysis and comparison between companies using different methods.

Balance Sheet Effects

The primary impact on the balance sheet is in the valuation of inventory (a current asset) and, consequently, retained earnings (part of equity). Under FIFO, the ending inventory reflects the most recently purchased goods, typically at more current market prices. Conversely, LIFO values ending inventory using the oldest costs, potentially understating its value on the balance sheet, especially during periods of inflation. This difference in inventory valuation directly impacts the total assets reported. The effect on retained earnings is indirect; a lower inventory value under LIFO leads to a higher cost of goods sold, reducing net income, and thus reducing retained earnings.

Income Statement Effects

The most pronounced impact of the choice of inventory costing method is on the income statement. During periods of inflation, LIFO generally results in a higher cost of goods sold because the most recently purchased (and most expensive) goods are assumed to be sold first. This leads to lower reported net income compared to FIFO. Conversely, FIFO reports a lower cost of goods sold during inflation, resulting in higher net income. In deflationary periods, the effects are reversed. The differences in reported net income can be substantial, impacting key financial ratios like gross profit margin and profitability. For example, a company experiencing rising inflation might show a lower net profit margin under LIFO than under FIFO, potentially affecting investor perception and creditworthiness.

Cash Flow Statement Effects

The impact on the cash flow statement is less direct but still significant. While the operating activities section is indirectly affected by the changes in net income (as discussed above), the investing activities section remains largely unaffected. The differences in net income arising from the choice of inventory method ultimately affect the cash flow from operating activities. A lower net income under LIFO (during inflation) will generally result in lower reported cash flow from operations, although this is not a direct, proportional relationship. Other factors, such as changes in accounts receivable and payable, also influence the cash flow statement. For instance, a company might experience higher cash inflows from operations under FIFO due to higher reported net income, even though the actual cash received from sales may be similar under both methods.

Final Thoughts

Ultimately, the choice between FIFO and LIFO hinges on a company’s specific circumstances and objectives. While FIFO provides a more intuitive representation of inventory flow and is often preferred under international accounting standards, LIFO can offer tax advantages during inflationary periods. A thorough understanding of both methods, along with a careful consideration of the potential implications for financial reporting and tax liabilities, is essential for making an informed decision. This exploration should equip you with the knowledge to navigate the complexities of inventory accounting and choose the most appropriate method for your specific needs.

Answers to Common Questions

What is the impact of inventory obsolescence on FIFO and LIFO?

Inventory obsolescence affects both methods by reducing the value of ending inventory. However, the impact on cost of goods sold differs; FIFO’s cost of goods sold reflects the older, potentially obsolete, inventory first, while LIFO’s reflects the newer inventory.

Can a company switch between FIFO and LIFO methods?

Generally, yes, but changes must be consistently applied and disclosed in the financial statements. Accounting standards may place restrictions on switching methods.

Which method is preferred under IFRS?

IFRS generally prohibits the use of LIFO. FIFO is the most commonly used method.

How does the choice of inventory method affect a company’s tax liability?

During inflationary periods, LIFO generally results in a higher cost of goods sold and therefore lower taxable income. The opposite is true during deflationary periods.

Remember to click How to Manage Accounts Payable and Accounts Receivable to understand more comprehensive aspects of the How to Manage Accounts Payable and Accounts Receivable topic.