The Role of Accounting in Mergers and Acquisitions is paramount, acting as the bedrock upon which successful transactions are built. From the initial due diligence phase, meticulously scrutinizing financial statements to uncover potential pitfalls, to the intricate process of purchase price allocation and the subsequent integration of disparate accounting systems, accounting expertise is indispensable. Understanding the financial health of target companies, navigating complex tax implications, and accurately forecasting the combined entity’s future performance all rely heavily on sound accounting principles and practices. This exploration delves into the multifaceted role of accounting, providing insights into its critical contributions to the success or failure of mergers and acquisitions.

This comprehensive overview will examine the various stages of the M&A lifecycle where accounting plays a crucial role. We will explore how accounting professionals verify financial health, allocate purchase prices, integrate accounting systems post-merger, ensure compliant financial reporting, and optimize tax implications. The analysis will incorporate real-world examples and best practices to illustrate the practical applications of accounting principles within this complex financial landscape.

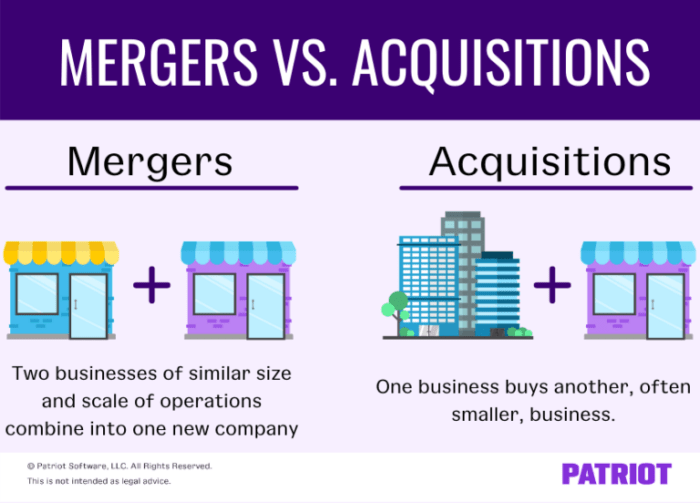

Due Diligence and Valuation: The Role Of Accounting In Mergers And Acquisitions

Accounting plays a pivotal role in mergers and acquisitions (M&A), particularly during the due diligence phase and subsequent valuation process. A thorough understanding of the target company’s financial health is crucial for making informed decisions and mitigating potential risks. Accurate financial information is the foundation upon which successful M&A transactions are built.

The due diligence process involves a comprehensive examination of the target company’s financial statements, internal controls, and operational aspects. Accountants are instrumental in verifying the accuracy and reliability of this information, ensuring that the buyer has a clear picture of the target’s financial position and future prospects. This detailed analysis helps determine a fair purchase price and identifies potential problems that could affect the deal’s success.

Assessing Financial Statement Accuracy

Accountants employ various methods to assess the accuracy and reliability of financial statements. These methods include analytical procedures, such as comparing financial ratios to industry benchmarks and analyzing trends over time. They also perform detailed testing of account balances, examining supporting documentation to verify the accuracy of reported transactions. Furthermore, they evaluate the target company’s internal controls to assess the reliability of its financial reporting processes. Weaknesses in internal controls can indicate a higher risk of material misstatements in the financial statements.

Examples of Accounting Irregularities

Several common accounting irregularities or inconsistencies might be uncovered during due diligence. For instance, revenue recognition issues, where revenue is improperly recognized before it’s earned, can significantly inflate a company’s apparent profitability. Similarly, aggressive accounting practices related to inventory valuation, such as overstating inventory levels, can artificially boost reported assets and profits. Unidentified contingent liabilities, such as pending lawsuits or environmental remediation costs, represent significant risks that can materially impact the valuation. These irregularities can lead to a downward adjustment in the valuation of the target company, potentially causing the deal to be renegotiated or even abandoned.

Valuation Methodologies and Accounting Data Needs

Different valuation methodologies rely on different aspects of accounting data. The following table illustrates this relationship:

| Valuation Methodology | Description | Accounting Data Needs | Strengths |

|---|---|---|---|

| Discounted Cash Flow (DCF) | Projects future cash flows and discounts them back to their present value. | Historical financial statements (income statement, balance sheet, cash flow statement), projected financial statements, cost of capital. | Theoretically sound, considers future growth potential. |

| Precedent Transactions | Compares the target company to similar companies that have recently been acquired. | Financial statements of comparable companies, transaction details (purchase price, terms). | Market-based, relatively simple to apply. |

| Market Multiples | Uses ratios such as price-to-earnings (P/E) or enterprise value-to-EBITDA to estimate the target company’s value. | Financial statements of comparable companies, market data (stock prices, market capitalization). | Relatively simple, readily available data. |

| Asset-Based Valuation | Estimates the value of the target company’s net assets. | Balance sheet, detailed asset and liability schedules, market values of assets. | Useful for companies with primarily tangible assets, less reliant on future projections. |

Purchase Price Allocation (PPA)

Purchase Price Allocation (PPA) is a crucial step in the post-merger integration process. It involves systematically assigning the total purchase price to the individual assets and liabilities acquired in a business combination. This process is governed by accounting standards, primarily IFRS 3 and ASC 805, and has significant implications for future financial reporting and tax liabilities. Accurate PPA ensures the fair reflection of the acquired business’s financial position on the acquirer’s balance sheet.

The process begins with identifying all assets and liabilities acquired. This requires a thorough understanding of the target company’s operations, contracts, and legal structure. Each identified asset and liability is then assigned a fair value, representing the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The sum of these fair values should equal the total purchase price. Any difference is recognized as goodwill, an intangible asset representing the future economic benefits arising from synergies and other non-identifiable assets. It is crucial to remember that the fair value determination must adhere to specific accounting standards and often involves significant professional judgment, especially concerning intangible assets.

Discover how How to Record and Manage Business Liabilities has transformed methods in this topic.

Methods for Allocating Purchase Price

Different methods can be employed to allocate the purchase price, each with its own impact on future financial reporting and tax implications. The most common approach involves using a combination of market-based valuation techniques (e.g., comparable company analysis, discounted cash flow analysis) and other valuation approaches. The choice of method depends on the nature and characteristics of the acquired assets and liabilities. For example, tangible assets like property, plant, and equipment might be valued using market prices or appraisal methods, while intangible assets such as brand names or customer lists might require more complex valuation models. The allocation ultimately aims to reflect the fair value of each individual asset and liability. Inconsistent or poorly supported allocations can lead to material misstatements in financial statements and trigger regulatory scrutiny.

Fair Value Determination of Intangible Assets

Determining the fair value of intangible assets is often the most challenging aspect of PPA. Intangible assets are inherently difficult to value because their value is not directly observable in the market. For example, determining the fair value of a brand name or customer relationships requires the use of sophisticated valuation techniques such as income approaches, market approaches, or cost approaches. These techniques often rely on assumptions and estimations, increasing the complexity and potential for error. The selection of appropriate valuation techniques and the reasonableness of the underlying assumptions are crucial to ensure the reliability of the PPA. The valuation process must be thoroughly documented and justified to support the final allocation. Discrepancies or lack of robust supporting documentation can lead to significant accounting challenges and potential regulatory issues. For example, an overvaluation of an intangible asset could lead to an overstatement of assets and an understatement of goodwill, affecting future impairment testing and financial reporting.

Best Practices for Documenting and Supporting the PPA Process

Comprehensive documentation is essential for a successful PPA process. This documentation should clearly Artikel the methodology used, the underlying assumptions, and the supporting evidence for the fair value estimations. The documentation should be detailed enough to allow for independent verification and scrutiny by auditors and regulators. Best practices include:

- Detailed valuation reports prepared by qualified professionals.

- Clearly defined valuation methodologies and assumptions.

- Comprehensive supporting documentation for all valuation inputs.

- Regular reviews of the PPA throughout the integration process.

- Internal controls to ensure the accuracy and completeness of the data used in the PPA.

Adherence to these best practices minimizes the risk of errors and ensures compliance with accounting standards, ultimately leading to a more reliable and transparent financial reporting process. A well-documented PPA also facilitates smoother audits and reduces the potential for disputes with tax authorities. A robust PPA process, therefore, is not merely a compliance exercise but a critical component of successful post-merger integration.

Post-Merger Integration

Post-merger integration (PMI) is a critical phase following a merger or acquisition, significantly impacting the long-term success of the combined entity. Effective integration of accounting systems and processes is paramount to achieving synergies, optimizing operations, and ensuring accurate financial reporting. This section explores the key accounting considerations during PMI.

Comparing Accounting Systems for Integrated Entities

Choosing the right accounting system post-merger is crucial. Several factors influence this decision, including the size and complexity of both entities, existing IT infrastructure, and the desired level of integration. A large company acquiring a smaller one might opt to integrate the smaller company’s systems into its own, while two similarly sized companies may consider a more collaborative approach, potentially selecting a new, neutral system. Different systems offer varying degrees of scalability, functionality, and compatibility. Cloud-based systems, for example, often provide greater flexibility and scalability than on-premise solutions, particularly beneficial for rapidly growing organizations. Legacy systems, while familiar, might lack the capacity or features needed to support the expanded operations of the merged entity. A thorough assessment of each system’s capabilities and limitations is essential before making a selection.

Consolidating Financial Statements Post-Merger

Consolidating financial statements after a merger involves combining the financial information of the acquiring and acquired companies into a single set of statements. This process requires adjustments to account for differences in accounting policies, currency conversions (if applicable), and the elimination of intercompany transactions. The consolidation process adheres to generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS), depending on the jurisdiction. For example, goodwill, arising from the difference between the purchase price and the net fair value of identifiable assets acquired, is recognized on the consolidated balance sheet. The consolidated income statement reflects the combined revenues and expenses of both entities, while the consolidated cash flow statement shows the overall cash flows of the merged company. This detailed process ensures a comprehensive and accurate financial picture of the post-merger entity.

Integrating Accounting Processes and Controls Post-Acquisition

Integrating accounting processes and controls post-acquisition is a multifaceted undertaking. A structured, phased approach is typically recommended. This involves a detailed assessment of the existing accounting processes and controls of both companies, identifying areas of overlap, redundancy, and potential conflict. Standardization of accounting policies, chart of accounts, and reporting procedures is a key step. This might involve migrating to a single accounting system or adapting existing systems to align with a common framework. Robust internal controls, including segregation of duties, authorization procedures, and regular reconciliations, need to be established to mitigate risks and ensure accuracy. Furthermore, post-acquisition audits are often conducted to verify the accuracy of financial records and assess the effectiveness of the integrated accounting system. This comprehensive approach guarantees consistent and reliable financial reporting for the newly formed entity.

Tracking Acquired Business Performance and Identifying Areas for Improvement

Post-acquisition, effective tracking of the acquired business’s performance is crucial for realizing the anticipated synergies. The integrated accounting system provides the necessary data to monitor key performance indicators (KPIs) such as revenue growth, profitability margins, and return on investment (ROI). Regular reporting and analysis of this data allow management to assess the success of integration efforts and identify areas needing improvement. For instance, variances from projected performance can be investigated to pinpoint operational inefficiencies or strategic misalignments. This data-driven approach enables proactive intervention, maximizing the value of the acquisition and ensuring the long-term success of the merged entity. By comparing pre- and post-acquisition performance, managers can measure the impact of integration initiatives and adjust strategies as needed. This continuous monitoring and improvement cycle is critical for achieving the full potential of the merger.

Financial Reporting and Disclosure

Mergers and acquisitions (M&A) significantly impact a company’s financial position and performance, necessitating meticulous financial reporting and disclosure. Accurate and transparent reporting is crucial for investors, creditors, and regulatory bodies to understand the transaction’s effects and the combined entity’s financial health. This section Artikels the accounting requirements and the necessary disclosures under relevant accounting standards like IFRS and GAAP.

Accounting Requirements for Reporting Mergers and Acquisitions

The accounting treatment of M&A transactions depends on the acquisition method used. Under IFRS and GAAP, the acquisition method is generally applied when one entity obtains control over another. This involves recognizing the identifiable assets acquired, liabilities assumed, and any non-controlling interests at their fair values at the acquisition date. The difference between the consideration transferred and the net fair value of the identifiable assets and liabilities acquired is recognized as goodwill (or a gain if the fair value exceeds the consideration). Pooling of interests, a method previously used, is largely obsolete under current accounting standards. The specific requirements for recognizing and measuring the various elements of an acquisition are detailed in IFRS 3 and ASC 805 (US GAAP).

Reflection of Mergers and Acquisitions in Financial Statements

Mergers and acquisitions significantly impact a company’s financial statements. The balance sheet reflects the changes in assets, liabilities, and equity resulting from the acquisition. Assets acquired are added, liabilities assumed are recorded, and equity changes depending on the acquisition method and the form of consideration. The income statement will show the combined revenue and expenses of the merging entities. Post-acquisition adjustments, such as amortization of acquired intangible assets, will also impact the income statement. The cash flow statement will reflect the cash outflows used to finance the acquisition and any cash inflows or outflows resulting from the integration process. For example, a company acquiring another might show an increase in property, plant, and equipment (PP&E) on the balance sheet and an increase in goodwill as an intangible asset. The income statement will reflect the revenue and expenses of the acquired company after the acquisition date.

Disclosures Regarding Goodwill, Intangible Assets, and Other Acquisition-Related Items, The Role of Accounting in Mergers and Acquisitions

Significant disclosures are required regarding goodwill, intangible assets, and other acquisition-related items. Goodwill, representing the excess of the purchase price over the net fair value of identifiable assets and liabilities, must be disclosed separately on the balance sheet. Impairment testing of goodwill is also required periodically. Intangible assets acquired, such as patents, trademarks, and customer relationships, must be identified and amortized over their useful lives. Detailed information about the fair value determination of assets and liabilities, the allocation of the purchase price, and any contingent consideration must also be disclosed in the financial statements’ notes. For instance, a company might disclose the estimated useful life and amortization method used for acquired software licenses.

Key Financial Reporting Considerations for M&A Transactions

Before, during, and after an M&A transaction, several key financial reporting considerations are crucial. These include:

- Accurate valuation of assets and liabilities.

- Appropriate allocation of the purchase price.

- Proper recognition and measurement of goodwill and intangible assets.

- Compliance with relevant accounting standards (IFRS or GAAP).

- Disclosure of all material information relating to the transaction.

- Post-acquisition accounting adjustments and subsequent impairment testing.

- Internal controls to ensure accurate and reliable financial reporting.

Failing to address these considerations can lead to inaccurate financial reporting, regulatory scrutiny, and potential legal ramifications. Thorough planning and coordination between accounting and legal teams are vital to ensure compliance and transparency.

Tax Implications

Mergers and acquisitions (M&A) transactions have significant tax implications for both the acquiring and target companies. Understanding these implications is crucial for effective planning and minimizing overall tax liabilities. Accounting professionals play a vital role in navigating the complex tax landscape associated with M&A, ensuring compliance and optimizing tax outcomes.

The tax implications of M&A are multifaceted, encompassing various tax jurisdictions and varying tax rates. A comprehensive understanding of these implications requires expertise in both accounting and tax law. Failure to adequately address tax considerations can lead to substantial financial penalties and jeopardize the success of the transaction.

Income Tax Implications

The acquisition structure significantly impacts income tax liability. For example, a stock purchase generally results in the target company’s assets and liabilities carrying over their existing tax basis, while an asset purchase allows the buyer to establish a new tax basis for the acquired assets. This difference affects depreciation and amortization deductions, influencing future tax liabilities. Furthermore, the allocation of the purchase price among various assets and liabilities impacts the depreciation schedule and subsequent tax deductions. Careful planning is essential to maximize depreciation and amortization benefits and minimize future tax burdens. An example of this would be the difference in tax treatment of goodwill under US GAAP and IFRS, which impacts the timing and amount of tax deductions.

Capital Gains Taxes

Shareholders of the target company may realize capital gains upon the sale of their shares in an acquisition. The tax rate on these gains depends on factors such as the holding period of the shares and the shareholder’s tax bracket. Accounting professionals help determine the capital gains realized by shareholders, preparing necessary tax documentation and ensuring compliance with all relevant tax regulations. The acquisition structure, again, plays a crucial role. A stock purchase generally leads to capital gains taxes for the target company’s shareholders, while an asset purchase might trigger different tax consequences depending on the type of assets involved. Accurate valuation of the acquired assets is critical for determining the appropriate capital gains tax liability.

Other Relevant Taxes

Beyond income and capital gains taxes, other taxes may apply in M&A transactions, including state and local taxes, sales taxes, and transfer taxes. The specific taxes vary depending on the location of the companies involved and the nature of the transaction. For instance, state franchise taxes could be affected by the change in ownership and the resulting change in the state of incorporation. Accounting professionals must ensure compliance with all applicable tax regulations, carefully considering the impact of these taxes on the overall transaction cost and profitability. A thorough due diligence process, involving detailed analysis of the target company’s tax liabilities, is crucial for identifying potential tax risks and opportunities.

Tax Planning and Optimization

Accounting professionals use accounting data to identify and implement tax planning strategies that minimize tax liabilities. This includes structuring the transaction to maximize depreciation deductions, optimizing the allocation of the purchase price, and utilizing various tax credits and incentives. For example, they might recommend structuring the deal as a tax-free reorganization to avoid immediate capital gains tax liabilities for the target company’s shareholders. Accurate accounting records are vital for supporting tax filings and audits, providing clear documentation of the transaction’s financial aspects and ensuring compliance with tax regulations. Detailed financial statements, including balance sheets, income statements, and cash flow statements, are crucial in supporting tax computations and justifying tax positions.

Use of Accounting Data in Tax Filings and Audits

Accounting data forms the bedrock of tax filings and audits related to M&A activities. Detailed financial statements, transaction records, and supporting documentation are crucial for demonstrating compliance with tax regulations and justifying tax positions. For example, the allocation of the purchase price to different assets and liabilities, as reflected in the purchase price allocation (PPA), directly impacts the depreciation deductions claimed and, consequently, the tax liability. Accurate accounting data is essential for substantiating this allocation and ensuring its compliance with tax laws. During tax audits, accounting professionals use this data to defend the company’s tax positions and demonstrate the accuracy of the tax filings. This includes providing detailed explanations of accounting methodologies used and reconciling discrepancies between accounting records and tax returns.

Financial Forecasting and Budgeting

Financial forecasting and budgeting are critical processes following a merger or acquisition. They provide a roadmap for the combined entity’s future financial performance, allowing management to make informed decisions regarding resource allocation, investment strategies, and overall operational efficiency. Accurate forecasting relies heavily on the detailed accounting data gathered during due diligence and the subsequent integration of the acquiring and acquired companies’ financial systems.

The accounting data from both entities, including historical financial statements, operational budgets, and sales forecasts, forms the foundation for developing a comprehensive financial forecast for the combined entity. This involves consolidating the financial information, adjusting for any identified synergies or redundancies, and projecting future performance based on various assumptions about market conditions, economic growth, and internal operational efficiencies. For example, revenue synergies might be projected from cross-selling opportunities between the two companies’ product lines, while cost synergies might arise from eliminating redundant administrative functions or leveraging economies of scale in procurement. These projections are then used to create a detailed operating budget that Artikels the expected revenue, expenses, and profitability for the combined entity over a specified period, typically one to three years.

Challenges in Integrating Forecasting and Budgeting Systems

Integrating different forecasting and budgeting systems post-merger presents significant challenges. Differences in accounting methodologies, software platforms, and organizational structures can create inconsistencies and delays. For example, one company might use a top-down budgeting approach, while the other uses a bottom-up approach, leading to conflicts and inaccuracies in the consolidated budget. Data reconciliation becomes a complex task, requiring careful analysis and adjustment to ensure consistency and accuracy across different systems and accounting periods. Furthermore, cultural differences between the two organizations can also impact the successful integration of budgeting processes, as different teams may have different levels of familiarity and comfort with specific software or methodologies. A standardized process, comprehensive training, and effective communication are essential to overcome these challenges.

Key Financial Metrics for Post-Acquisition Performance Monitoring

Several key financial metrics should be tracked diligently after an acquisition to monitor performance and ensure that the merger is achieving its intended goals. These metrics should be carefully selected to reflect the specific objectives of the merger and the nature of the combined business.

- Revenue Growth: Tracking overall revenue growth, as well as growth in specific product lines or geographic regions, provides insights into the success of integration and market penetration.

- Cost Synergies Realization: Monitoring the realization of cost synergies, such as reduced administrative expenses or improved procurement costs, is crucial for evaluating the financial benefits of the merger.

- Profitability Margins: Analyzing gross profit margin, operating margin, and net profit margin helps assess the overall profitability of the combined entity and identify areas for improvement.

- Return on Investment (ROI): Tracking ROI on the acquisition helps evaluate the financial return of the investment and ensures alignment with the initial investment thesis.

- Earnings Per Share (EPS): Monitoring EPS helps assess the impact of the acquisition on shareholder value.

- Working Capital Management: Efficient working capital management is essential for maintaining liquidity and ensuring smooth operations. Key metrics include days sales outstanding (DSO), days payable outstanding (DPO), and inventory turnover.

Creating a Post-Merger Financial Forecast Incorporating Synergies and Cost Savings

Developing a post-merger financial forecast that accurately reflects the anticipated synergies and cost savings requires a careful and systematic approach. It begins with a thorough assessment of the individual companies’ financial performance, followed by an identification and quantification of potential synergies and cost savings.

For instance, consider a scenario where Company A acquires Company B. Company A’s historical revenue is $100 million, and Company B’s is $50 million. Through detailed analysis, it’s determined that revenue synergies of $10 million can be achieved through cross-selling opportunities and expanded market reach. Furthermore, cost synergies of $5 million are anticipated through eliminating redundant administrative functions and leveraging economies of scale in procurement.

The forecast would then incorporate these synergies. The combined revenue would be $160 million ($100M + $50M + $10M), and the cost savings would be reflected in a reduction of operating expenses. This would result in a higher projected net income compared to a simple summation of the individual companies’ projected income statements. Detailed financial models, often using spreadsheet software, are employed to simulate different scenarios and test the sensitivity of the forecast to various assumptions. Regular monitoring and adjustments are crucial to ensure the forecast remains aligned with actual performance. This iterative process allows management to adapt to changing market conditions and internal operational realities, ultimately optimizing the financial performance of the merged entity.

Last Recap

In conclusion, the role of accounting in mergers and acquisitions extends far beyond simple bookkeeping. It is a critical function that permeates every stage of the process, from initial valuation and due diligence to post-merger integration and ongoing financial reporting. Mastering the complexities of accounting within the M&A context is crucial for mitigating risk, maximizing value, and ensuring the long-term success of the combined entity. A thorough understanding of accounting principles and their application throughout the M&A lifecycle is not merely advantageous; it is essential for achieving a successful and profitable outcome.

Common Queries

What are some common accounting irregularities found during due diligence?

Common irregularities include misstated revenue, hidden liabilities, improperly capitalized expenses, and inconsistencies in accounting methods.

How does purchase price allocation affect future tax liabilities?

PPA impacts future tax liabilities by determining the tax basis of acquired assets and liabilities, influencing depreciation, amortization, and other tax deductions.

What are the key challenges in integrating accounting systems post-merger?

Challenges include differences in accounting software, chart of accounts, and internal controls, requiring significant time and resources for reconciliation and standardization.

What are some key financial metrics to track post-acquisition?

Key metrics include revenue growth, profitability margins, return on investment, and efficiency ratios of the acquired business.